read our blog

get the latest updates from our firm in our blog updates

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

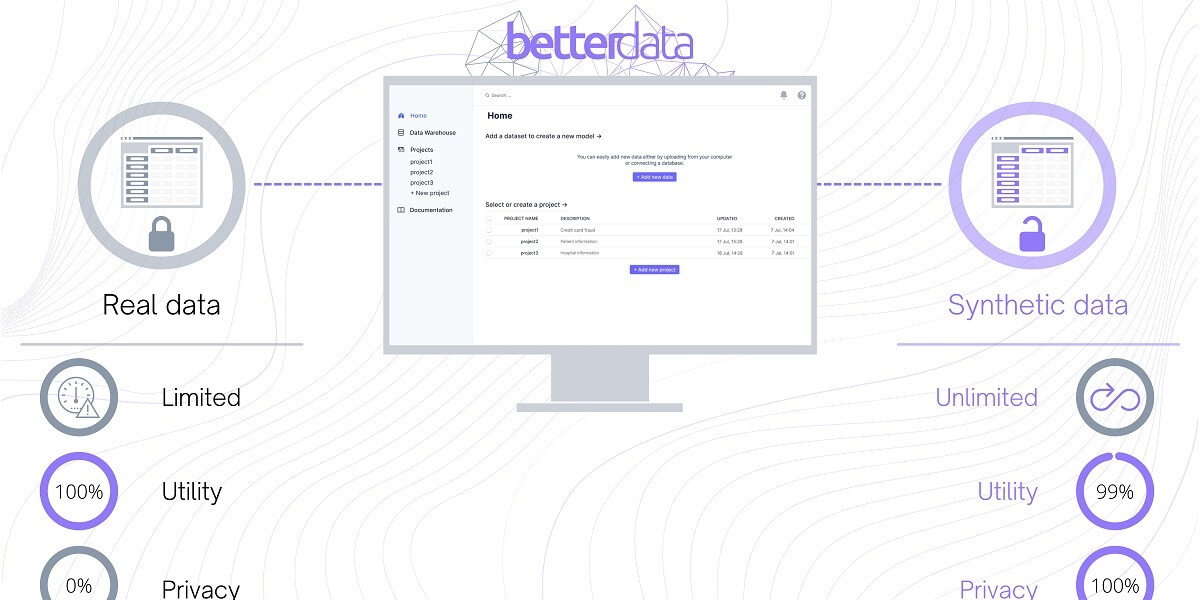

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.

Kindrik Partners advised Singapore-based startup Green Li-ion on its recent USD20.5 million pre-B funding round. The round was led by TRIREC, followed by investors including Banpu NEXT and Equinor Ventures.

Green Li-ion was founded in 2020 by Leon Farrant and Reza Katal to develop technology capable of recycling lithium-ion batteries and is now a leading developer of battery recycling technology. The company has developed modular units capable of recycling spent batteries into cathode material that can be used in the production of new batteries. Each unit is able to process 4-6 metric tons of spent batteries per day, the equivalent of 20 EV batteries or 70,000 iPhones.

The funding will help the company scale its manufacturing capacity in order to deliver 50 modular units per year. The first commercial operation is slated to start production in the first half of 2023 in Oklahoma, USA.

As technology lawyers we have worked with hundreds of companies raising their first equity financing round. We have also come across companies and founders (typically on their next financing round) who completed their seed rounds without using a lawyer.

Proceeding without a lawyer is understandable for early stage tech companies. Venture capital term sheets and long form documents are often presented as standard form agreements. The perception is that engaging a lawyer will add time and cost to a process when getting money in the door and keeping costs low are key considerations.

We may be slightly biased(!), but companies and founders who we have worked with had an easier time closing their fundraising quickly and efficiently. They were also in a much better position following closing and when raising their next funding round. Here are 5 reasons why engaging a lawyer on your first round is important, and some good news on the cost.

more efficient process

Closing an equity financing is often a company’s first experience with a legal process. The round will involve negotiating and executing a term sheet, subscription agreement, shareholders’ agreement, updated constitution, and disclosure letter, along with ancillary documents such as director and shareholder resolutions and waivers.

Having a lawyer to guide the company and founders through this process is critical to getting the round closed as efficiently as possible. Some documents (like the disclosure letter and the updated constitution) are usually prepared on the company side, and others (like resolutions and the investor KYC process) can be prepared in advance with your lawyer liaising with your company secretary, meaning that they don’t hold up signing and closing.

making sure you have market terms

Because we advise on many capital raises, we understand how the material terms of your capital raise compare with what we see as the market standard for seed rounds. This provides founders with comfort on which terms they can regard as standard and which to negotiate. If sticking points arise, we can also suggest ways to resolve them.

We are also familiar with most of the seed investors in Singapore, their documentation, and their expected positions on most items. We find this also makes a big difference in streamlining the drafting and negotiation processes.

understanding your obligations

The venture capital terms and documentation from institutional investors in Singapore are typically of a high quality, and are becoming more standardized across the ecosystem. However, these agreements still include important representations, warranties and undertakings from the company, and in certain cases founders personally. Most of these will be familiar to VCs and other experienced parties, but it is important for founders (especially first timers) to understand what these items mean, and the best way to mitigate any risk.

Broadly speaking these items can be categorised as:

- representations and warranties provided by the company and (usually) founders about the position of the company at the time of investment

- restrictions on the actions of the company and founders going forward, such as investor veto rights (also known as reserved matters), the vesting of founder shares against their continued involvement in the company, and restrictions on the transfer of founder shares (usually lock-in, rights of first refusal, and co-sale rights)

- ongoing positive obligations to the investors, most commonly information and reporting obligations.

Understanding these obligations is important, not just to avoid a technical breach of the company’s governance documents, but also to maintain good relationships with your investors.

Post-closing requirements

Seed round documents usually include one or two post-closing obligations on the company. Most commonly tidying up any items raised during due diligence that could not be dealt with before closing, and/or the establishment of an ESOP.

In the excitement of closing a seed round it can be easy to forget these post-closing matters and, in the absence of a lawyer, this is often not picked up until the due diligence process for the company’s next round. This can create delays in order to address these items before moving ahead with a new investment round.

Having a lawyer will help founders to stay on top of these obligations.

good position moving forward

A company’s seed round investment documents will usually be terminated and replaced at the time of the company’s series A round. However, incoming series A investors will review those documents as part of their due diligence. If those seed documents include terms that are unusually favourable for investors (like a non-standard liquidation preference), your incoming investors may expect the same to be included in your series A agreements. Similarly, your seed investors may reasonably expect to retain their existing rights in the next round documentation (or in some cases your seed investor may even be leading your series A round). It is important that your seed documents are not placing the company in a potentially difficult position for negotiating future funding rounds.

but what about the cost?

We are always excited to assist startups with their seed rounds. These rounds are often a company’s first time accessing a material amount of external capital and represent a major milestone in the company’s life cycle.

To help keep your costs under control at this early stage, we offer a fixed fee of S$6,500 to work with you on your seed round subject to certain conditions. You can read more about our fixed fee offer here. Even if our fixed fee offer does not apply to your circumstances, we are happy to discuss your round and provide an estimate before kicking off.

Back in 2018, Y-Combinator (YC) updated their core investment instrument and launched what is now known as the post-money SAFE.

We analysed the post-money SAFE back in 2020 – see our blog here https://kindrik.co.nz/blogs/a-primer-on-post-money-safes-in-new-zealand/. The main difference between a pre-money and post-money SAFE is that, on conversion, under the pre-money terms the calculation of the number of conversion shares does not include the conversion of the SAFE itself and any other convertible instruments in issue (other convertible securities). With a post-money SAFE all of these other convertible securities are included. The end result is further dilution for existing ordinary shareholders on conversion of the post-money SAFE.

But what about convertible notes? Have they remained drafted on a pre-money basis or, like the SAFE, has the market moved towards the more investor friendly post-money position?

Convertible notes v SAFEs

The terms of convertibles notes differ from SAFEs. SAFEs remain outstanding until a conversion event occurs, or the company has a liquidity event. So, in effect, there is no repayment obligation. In contrast, convertible notes have a maturity date and generally accrue interest. Therefore, startups have no time pressure to close an equity financing under a SAFE. Whereas under a convertible note, they might need to get it done within say 18 months, or the note could be repayable. For that reason, SAFEs are generally the preferred document for founders.

The market has certainly followed YC’s lead when it comes to SAFEs. Most SAFEs we now see are the post-money version. However, the same can’t be said for convertible notes, for which conversion into shares is still calculated on the more founder friendly pre-money calculation. Looking at templates available online, whether provided by law firms (including our own!), VCs or industry bodies, this looks to be the consistent approach across the board. That said, we do occasionally see them on deals where investors are looking to secure a better position or when they simply draft the document incorrectly.

Round up

Founders should be cautious here and take advice at the term sheet stage so there is no ambiguity when everyone comes to drafting the final instrument. If any post-money instrument is used, it may require founders to rethink the valuation cap on the deal.

Investors could argue that there is nothing intrinsically different between a SAFE and a convertible note in terms of how equity should be calculated on a conversion event. I.e. why shouldn’t the number of shares be determined on the same basis for each?

However, YC’s justification at the time of launching the new SAFE was that it makes the conversion calculation simpler and creates more certainty over the future dilution. Which is certainly true. But YC’s model is about speed and efficiency and they invest in multiple companies in their intakes. A SAFE is also a pretty founder friendly investment instrument, and rarely negotiated much. A convertible note, on the other hand, has other disadvantages to founders and more onerous terms, in particular, interest and repayment obligations. Notes also tend to include information rights, a most favoured nation clause, events of default provisions and other covenants that don’t typically appear in SAFEs.

Taking that into consideration, our view remains that convertible notes should be drafted on a pre-money basis, and that post-money notes remain non-market.

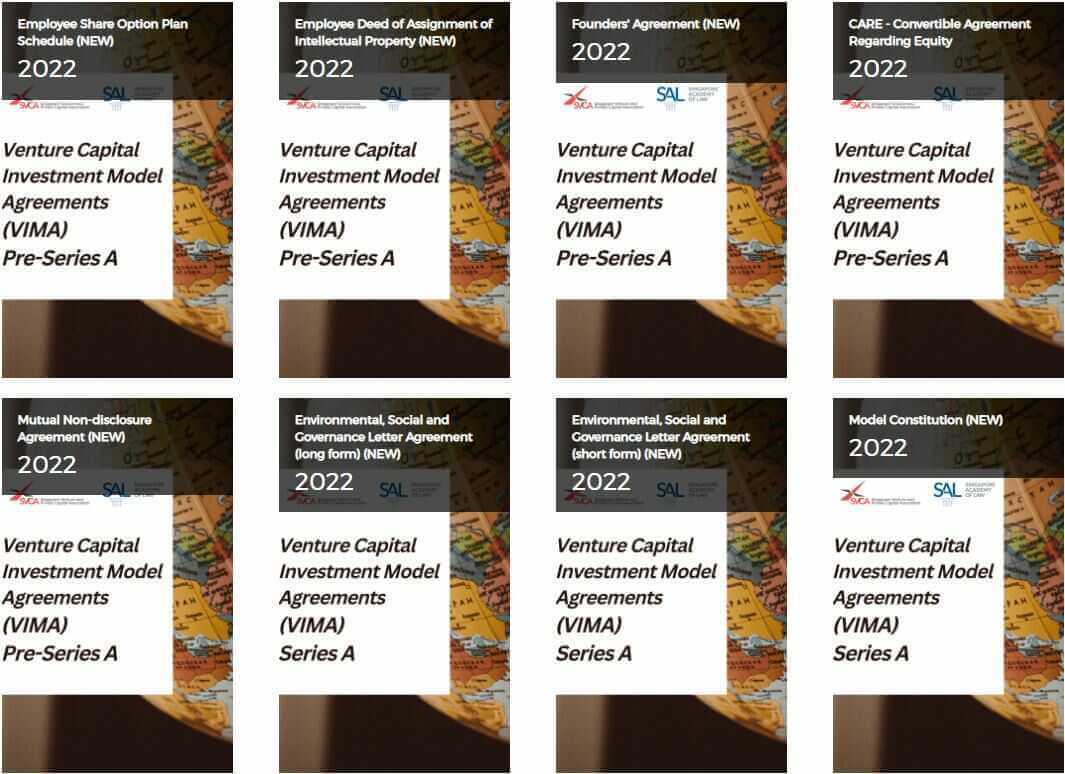

The template documents used in the venture capital ecosystem across Southeast Asia have been updated. Launched by the Singapore Academy of Law and the Singapore Venture & Private Capital Association in 2018, the new VIMA 2.0 documents are available for free to help start-ups.

8 new documents have been added to the suite of documents, including a founders’ agreement, a model constitution, an IP assignment, and an employee share option plan primer. The inclusion of a template letter covering Environmental, Social and Governance (ESG) matters reflects the increasing trend of investors to seek ESG commitments from their portfolio companies.

The core investment documents from 2018 have also been updated. This includes the two term sheet forms, the subscription agreement, and the shareholders’ agreement. We’ve summarised the main changes to these documents below (note this is non-exhaustive).

Term sheet (short form)

- clarifies that all parties bear their own costs

- provides that no dividends are to be paid to ordinary shareholders unless the holders of the preference shares either first or simultaneously receive a pro rata share of such dividends

- provides an option for the liquidation preference to be a multiple of original investment funds

- makes completion subject to customary conditions precedent

- expands the representations and warranties, including providing a general indemnity

- adds the option for pre-emptive rights to be provided to shareholders holding a certain percentage of shares

Term sheet (long form)

All changes made to the short form term sheet, plus it:

- adds clarification to the liquidation preference provision requiring that, if available proceeds are insufficient to make payments in full to preference shareholders on a liquidity event, the proceeds be shared among the holders of preference shares pro rata on an as-converted basis

- adds an optional provision to prohibit variation of the shareholders’ agreement unless agreed by all parties or by a certain % of shareholders

- lists certain new conditions precedent

Subscription agreement

- adds new default conditions precedent (clause 2 and schedule 4)

- includes new pre-completion undertakings (clause 3)

- changes the completion mechanics (clause 4.1)

- adds provisions detailing what happens if a single investor or the company fails to perform its obligations on completion – e.g., whether completion can occur with the other investors or not (clauses 4.4 and 4.5)

- adds a founder specific cap on liability (clause 8.4)

- allows an investor to assign or transfer its rights, benefits, interests and/or obligations to an affiliate

- adds new warranties covering items such as anti-money laundering, IP assignment by employees, and insolvency (schedule 6)

- includes a disclosure schedule that removes the need for a separate disclosure letter (schedule 8)

- removes the terms and conditions of the preference shares

Shareholders’ agreement

- adds further provisions governing meetings and shareholders (clause 3.2)

- adds vesting provisions covering good leaver and bad leaver scenarios (clause 16)

- limits the personal liability of the founders (clause 19)

- expands the termination provision so that it automatically terminates in certain situations (e.g. on an IPO). Termination does not release a party from accrued rights, obligations and liabilities (clause 21)

- adds a new schedule including the terms and conditions of the preference shares (schedule 3).

Round up

The amendments reflect changes commonly made by lawyers who use them on deals, and overall are an improvement. E.g., the new conditions precedent included in the subscription agreement are customary for equity financing transactions. The better place for the terms and conditions of the preference shares was arguably always in the shareholders’ agreement, as it is now. Including founder vesting provisions, caps on founder personal liability, and anti-corruption warranties/undertakings really just reflects market practice. The move to a disclosure schedule is also a good idea to remove the need for a separate letter.

There were some improvements that were missed. E.g., the tag along formula still does not reflect most tag along/co-sale provisions that we see in the market; and the liquidation preference language continues to require an actual conversion into ordinary shares (assuming proceeds come out higher on an as-converted basis), which would be avoided with more conventional drafting.

Kindrik Partners is delighted to have advised Hello Clever on its recent AUD4.5 million pre-seed and seed funding round led by Vectr Ventures. Other funders included Yolo Investments and CrossFund. Hello Clever is a buy-to-earn ecosystem startup founded in 2021 by business partners and friends Caroline Tran and Gavin Nguyen.

Through the Hello Clever App and the CleverShop, the company helps young Australians be “clever” with their money. Customers can shop, earn cashback, and make payments to friends in one place.

Given the economic difficulties being faced by businesses in 2022, co-founder Caroline says “we are lucky to still retain our position in the market with the ability to innovate, build new capabilities and secure long-term prospects while at the same time deliver the sustainable, profitable growth that our investors and business partners expect from us”.

Partner Chris Wilson says:

“The Hello Clever team clearly values its customers and their financial security, especially in the current uncertain economic environment. It was a pleasure working with such a pro-active and efficient founding team. We’re excited to see Hello Clever continue to grow and develop to help young people with their finances.”

The global economic downturn has inevitably hit the startup and venture capital ecosystem. Investors in startups, like everyone else, are impacted by falling stock prices and fund valuations, distracted from investing new money and busy supporting existing portfolio companies. These factors make it harder for startups to raise money right now.

But for those startups that are still raising money, what is the approach of investors? Is the VC term sheet about undergo a change?

valuations

Startup valuations are falling. For those companies that have raised a previous round of financing, founders will want to avoid a down round – a fundraising in which a company issues shares at a lower price than the previous investment round – at all costs, as doing so may trigger investors’ anti-dilution rights. If anti-dilution rights are triggered, founders could face significant further dilution.

If company cash is low, existing investors may need to support a new financing. If so, founders will need to negotiate hard with both new and existing investors. Anti-dilution rights can be fully or partially waived on a fundraising at the end of the day. If anti-dilution rights are triggered, founders may then need to ensure that they remain sufficiently incentivised following the dilution, for example via an increased portion of the company’s ESOP.

extension rounds and convertible notes

Extension rounds at the same price as the last financing round may be an alternative to a down round. With no increase in valuation, startups will want to classify such investments as a bridge or extension. Therefore, expect to see investment rounds using preference share class terminology such as series A2, series B+, pre-series A or similar.

We also anticipate more convertible notes will be used in the market. This not only avoids initial dilution but pushes the whole difficult discussion on current valuation to another day. This, of course, also has its disadvantages. To some extent, founders are just kicking the valuation debate down the road and it will still have to be addressed at some point. In the current market, it also seems inevitable that SAFEs will be less common than traditional convertible notes carrying repayment obligations. We also expect investors to be more aggressive on setting lower valuation caps and fluctuating price discounts depending on the timing of conversion into equity.

tranched investments

Now is the time to get money into the business to give it runway for a decent period of time. Tranched investments conditional on financial performance are best avoided by startups at the best of times. Right now, it is very difficult to forecast traction and performance over the next 12-18 months. Unfortunately, given the uncertain economic environment, investors may well think the opposite and insist on structuring investments in tranches subject to KPIs.

warrants

Warrants, which provide an option to purchase more shares at a future date at a fixed price, may also be a tool for investors to use in the current environment. The exercise price of such warrants is key – the lower the price, the more potential dilution. If warrants are issued and/or exercisable down the line, based on company performance, the true share price of the financing round may be considerably less than initially agreed.

redemption / buy-back rights

Investors sometimes include redemption or buy-back rights which entitle them to their money back in certain circumstances. Usually this is where there is some kind of event of default by the company or its founders.

However in difficult times, investors tend to broaden the circumstances in which such redemption or buy-back rights can be enforced (e.g. financial performance deteriorates or being unable to satisfy a key commercial arrangement or deliverable). In this uncertain economic period, investors may look to de-risk transactions even further using such a mechanism. Founders should be cautious about agreeing to any broad redemption or buy-back rights triggered by anything other than a material breach or default.

liquidation preference

Liquidation preferences provide investors with downside protection if a company is either sold or wound up. In such an event, investors are entitled to receive an agreed amount of the proceeds before anything is paid to other shareholders. During the good times, founders and startups have become accustomed to 1x non-participating liquidation preference in most cases – a generally accepted VC market standard. With stormy clouds above, we can expect that to change, with liquidation preference carrying higher multiples, and also participating preferences returning.

Further, for companies that have raised previous rounds of investment, incoming investors are more likely to seek a senior class of shares, than rank alongside existing preference shareholders, which is common in normal market conditions.

exit rights

Exit rights give investors a way to sell their shares if the company hasn’t got to a liquidity event (e.g. a trade sale or IPO) within a set period. We may see shorter time periods before these rights kick in. The remedies provided to investors vary, but we could see more instances of the following:

- a right to require the company to buy-back investors’ shares at a specified price (for example, based on fair market value)

- investors having the option to reconstitute the board giving them greater voting control

- an obligation on the board to engage an investment banker to find a buyer, coupled with a drag-along right so that shareholders (including founders) can be forced to sell at a price determined by investors

venture debt

Finally, venture debt is likely to become a more important source of financing in the short term, in most cases complementing an equity financing. As an alternative capital raising option for high growth companies, venture debt is a good option for entrepreneurs looking to extend their runway, using an instrument that results in less dilution.

round up

Right now VC firms and other investors will be taking a closer look at downside protection in their term sheets. Of course, not all investors are predatory, nor will the majority take advantage of the difficult economic climate to seek further influence in startups. But now is certainly the time for founders to reach out to lawyers at the term sheet stage to understand what is, and what isn’t, market standard, and how this may be changing.

Kindrik Partners advised edtech startup Jackett on its US$1 million seed funding round led by Forge Ventures. Entrepreneur First, Epic Angels Network, Carousell co-founder Siu Rui Quek, and OnLoop co-founder Projjal Ghatak also participated.

Charlotte Trudgill and Rachiket Arya started Jackett after realising that technology could enhance the teaching process, reduce the administrative burden on teachers, and create a more personalised experience for students. Jackett lets teachers scan and digitise questions, create personalised assessments using the platform’s library, and auto-grade students’ answers using AI. It also uses smart analytics to provide a deeper understanding of student performance over time.

Jackett plans to use the capital to improve its operating system and make its platform available to more teachers and education institutions in emerging markets.

Partner Chris Wilson says:

“Jackett has gone from strength to strength in its short history and this early involvement from prominent investors shows they have great potential going forward. We look forward to seeing them continue to help teachers deliver the best possible education to their students.”

Kindrik Partners is happy to have advised property technology company Propseller on its US$12 million series A round led by Vertex Ventures Southeast Asia and India.

Other participants in the round include existing investors Hustle Fund, Iterative, and Rapzo Capital, alongside new investors Partech, ICCP SBI, Vulpes Ventures and Redbadge Pacific. The fundraise also attracted investment from the co-founders of several prominent proptech companies, namely PropertyGuru’s Jani Rautiainen, Marta Higuera of OpenAgent, Steffen Wicker of Homeday and Flyhomes’ Tushar Garg.

Founded in 2018, Propseller has developed an end-to-end real estate transaction platform that has made transactions more efficient and data-driven for both buyers and sellers. Notably, the platform is able to tell users the likelihood of a successful closing at each step of the process.

Propseller plans to use its Series A funding to scale its business model, expand its offerings and enter overseas markets. To achieve this, it plans to significantly expand its current team of 50 employees by hiring 200 more people.

Partner Chris Wilson says:

“Buying a home is often the largest financial decision in a person’s life, and Propseller is revolutionising the way people buy and sell their homes by building a platform that prioritises efficiency and transparency. The company has modernised the traditional real estate agency and we look forward to seeing them bring these solutions to new markets.”

Kindrik Partners is delighted to have advised cleantech startup SunGreenH2 on its US$2 million seed funding round. The round was led by SGInnovate. Vinci BV, Entrepreneur First, SOSV’s HAX, she1K, and Apsara Investments also participated.

Founded in 2020, SunGreenH2 develops nanotechnology with the potential to transform hydrogen production. The company manufactures core components for electrolysers, which create hydrogen by splitting water molecules into their atom parts. SunGreenH2 has revolutionised this process by creating components that increase the production and decrease the energy consumption of electrolysers without relying on platinum and other expensive elements.

The funding will be used to set up their first manufacturing facility in Melbourne to meet the demands of their early partners. The company plans to partner with system integrators to produce whole electrolysis stacks and eventually with larger companies to produce more end-to-end solutions.

Partner Chris Wilson says:

“SunGreenH2 has the potential to be a pioneer in the production of green hydrogen production. We are pleased to be able to help the company secure this funding and look forward to seeing them contribute to a low-carbon future.”

Kindrik Partners is pleased to have advised cryptocurrency analytics platform Merkle Science on its US$24 million series A funding round. The round was co-led by BECO Capital, Darrow Holdings (an affiliate of Susquehanna International Group) and K3 Ventures.

Founded in 2018, Merkle Science develops threat detection, risk mitigation and compliance tools that can detect, investigate, and prevent cryptocurrency-related crime. The rapid adoption of blockchain technology across the financial sector, the escalating impact of hacks and greater regulatory scrutiny have resulted in a massive increase in demand for these tools.

The new investment will help Merkle Science expand in the USA and Europe, as well as fund the research and development of tools for emerging technologies such as NFTs, decentralised finance and cryptocurrency bridge protocols.

Partner Chris Wilson says:

“Despite some recent growing pain, there has been massive growth of the cryptocurrency market in recent years which has resulted in a significant increase in demand for improved security surrounding digital assets. Merkle Science has stepped up to provide multiple solutions in this area and we look forward to seeing how they will use this funding continue to contribute to the cryptocurrency industry.”

We’re pleased to have advised Philippine based e-commerce platform edamama on its US$20 million series A funding round led by Alpha JWC. Existing investors Gentree Fund, Robinson Retail Holdings, Innoven Capital, Kickstart Ventures and Foxmont Capital Partners also participated in the round.

edamama is a parenting-focused platform that offers customers a personalised shopping experience designed to simplify decision-making for parents. Following its launch in May 2020, the company has grown rapidly by providing families across the Philippines a safe and trustworthy way to digitally access an extensive range of parenting products through its proprietary technology. In addition to its innovative product offerings, edamama also provides an online gift registry and subscription services for essentials.

The company plans to use the funding to expand its operations, ramp up delivery solutions, and enhance its content and community. It also plans to open offline stores and scale its own private label portfolio.

Partner Lee Bagshaw says:

“edamama launched during the strict Covid lockdown imposed in the Philippines at a time where consumers were shifting from brick-and-mortar stores to e-commerce platforms. The business has continued to grow rapidly by establishing a reputation for providing affordable and quality products. We are delighted to have advised the company on their latest fundraise, one of the largest series A financings ever completed in the Philippines.”

Kindrik Partners is pleased to have advised digital B2B pharmacy platform SwipeRx on its US$27 million series B funding round led by MDI Ventures. Other investors in the round included the Bill & Melinda Gates Foundation, Johnson & Johnson Impact Ventures and Susquehanna International Group (SIG).

SwipeRx, formerly known as mClinica, was founded with the goal of providing tech-based solutions to issues facing pharmacies in Southeast Asia. SwipeRx pioneered the community-driven commerce model that unites the fragmented pharmacy channel on a single platform enabling them to access all the information, education and medicines they need. From online education, to centralised purchasing and logistics, to financing, SwipeRx caters to the critical needs of pharmacies.

Operating across Indonesia, the Philippines, Vietnam, Malaysia, Thailand and Cambodia, SwipeRx’s intends to further scale its growing network of pharmacies, expand specialised healthcare logistics to fulfil B2B commerce, accelerate its tech innovation and recruit talent

Partner Lee Bagshaw says:

“Pharmaceutical networks in Southeast Asia have long struggled with fragmentation, but SwipeRx’s platform is innovating how the industry operates via an innovative community-driven commerce model. We’re delighted to have advised the company on their latest financing and look forward to seeing how their innovation continues to transform the delivery of healthcare and pharmaceutical services.”

Kindrik Partners is delighted to have advised Filipino e-commerce platform GrowSari on its US$77.5 million series C financing. Investors in this round include the International Finance Corporation, KKR, Wavemaker Partners and the Temasek Group’s Pavilion Capital.

Founded in 2016, GrowSari is a B2B platform that provides support for micro, small, and medium-sized enterprises (MSMEs) in the country. GrowSari began as an ordering platform for sari-sari stores (small, independent convenience stores). Today, the platform provides many different types of MSMEs access to a wide range of digital services, including bill payments, telco reloads, wallet top-ups and procurement of retail goods and medicines.

The funding will allow GrowSari to continue to expand into new store formats, accelerate its national expansion and build its logistics and fulfillment network.

Partner Chris Wilson says:

“Small and medium sized-business play such a key role in the social and economic makeup of the Philippines, with MSMEs accounting for 63 percent of employment in the country. We are extremely pleased to help GrowSari continue to transform the way these companies do business”

Kindrik Partners is delighted to have advised Indonesian agritech start-up Sayurbox on its US$120 million series C financing led by Northstar and Alpha JWC Ventures. Other investors participating in the investment round included the World Bank’s International Finance Corporation, Astra Digital, Syngenta Group Ventures and Global Brain.

Founded in 2017, Sayurbox digitises Indonesia’s agricultural and food supply chain addressing inefficiencies in the industry. Using unique demand forecasting, inventory planning and route optimisation technology, the business increases customer experience through freshness, pricing, product range and delivery. Sayurbox currently serves around 1 million customers in the Greater Jakarta, Surabaya, and Bali areas, while working with more than 10,000 farmers nationwide, providing a seamless supply chain from the farm to the end consumer.

The investment will be used to accelerate growth in existing markets, expand to new cities and extend its end-to-end supply chain nationwide.

Partner Lee Bagshaw says:

“Agritech, logistics and food supply technology are rapidly growing sectors in Indonesia and Sayurbox leads the way in looking to improve productivity in a fragmented industry. We’re pleased to have been able to advise the company on this transformative financing round.”

We’re pleased to have advised Silent Eight on its US$40 million series B financing. The investment round was led by TYH Ventures and supported by HSBC Ventures, OTB Ventures, Wavemaker Partners, SC Ventures (Standard Chartered Bank’s venture unit), amongst others.

Silent Eight leverages AI to create compliance platforms for some of the world’s leading financial institutions. As a pioneer in the field of AI enhanced economic sanctions enforcement and financial crime prevention, its platform can investigate suspicious transactions, beneficiaries, and customers in real-time and at significant scale.

Founded in Singapore and operating in multiple markets, Silent Eight has raised US$55milion to date. The latest funding will be used to expand technology functions for its customers, and to hire over 150 data scientists, developers and engineers in 2022.

Partner Lee Bagshaw says:

Financial crime prevention is increasingly the most important topic for institutions and businesses. Artificial Intelligence systems such as Silent Eight’s that can operate rapidly and at scale, reducing manpower and cost, represent the future and we’d expect the business to continue to scale rapidly. Kindrik Partners is particularly delighted to have assisted on this substantial financing led by global investors.

Kindrik Partners is pleased to have advised digital financing platform Funding Societies on its US$144 million series C+ funding round. The investment round was led by SoftBank Vision Fund 2, with participation from VNG Corporation, Rapyd Ventures, EDBI, Indies Capital, K3 Ventures and Ascend Vietnam.

Funding Societies is the largest SME digital financing and debt investment platform in Southeast Asia. The company provides loans ranging from $500 to $1.5 million to small and medium-sized ranging from neighbourhood stores to high-growth start-ups. Since its launch in 2015, it has lent more than $2 billion in business financing via over 4.9 million loans.

Small and medium enterprises across Southeast Asia have historically struggled to access finance and Funding Societies has established itself as a key platform to provide sustainable finance for such businesses, utilising AI credit scoring technology.

The fundraising will enable further expansion beyond its current markets of Singapore, Indonesia (where it is known as Modalku), Malaysia and Thailand, with the Philippines now in Funding Societies sights. The capital raised will also enable further development of the technology platform.

Partner Lee Bagshaw says:

Digital financing platforms continue to scale rapidly as they serve the funding needs of SMEs in Southeast Asia. Funding Societies has grown rapidly in its seven years and is one of regions fintech stars. Kindrik Partners is therefore particularly delighted to have assisted on this latest venture financing round.

We’re delighted to have advised Singapore-based Appboxo on its US$7 million series A funding round led by RTP Global. Existing investors, Antler and 500 Global, together with new investors SciFi VC, Gradient Ventures also participated.

Appboxo’s platform lets developers convert their apps into super apps, either by building their own micro-apps or accessing them through their “showroom” marketplace for developers. The company is already used by 10 super apps across Southeast Asia, India and South Africa

The fundraising is intended to grow the business’s two products – Miniapp, a SaaS platform with SDKs and APIs for building and launching mini-apps and Shopboxo https://www.shopboxo.io/ which lets businesses set up and customise online stores via mobile.

Whilst Appboxo is currently focussing on Asia-Pacific, the intention is to enter new markets including Europe and the US. The company has scaled extremely fast in the last two years establishing new partnerships on the back of the significant growth in ecommerce and emergence of super apps in Southeast Asia.

We’re pleased to have advised Jala, an Indonesian aquaculture startup improving the sustainability of the shrimp farming sector, on their recent US$6 million seed round. The round was led by Althelia Sustainable Ocean Fund. Other participants in the round include the Meloy Fund, an American environmental conservation group; and Real Tech Fund, a Japanese deep-tech-focused fund.

Founded in 2015, Jala helps shrimp farmers manage their farm to increase their yield and create a sustainable farm. The proprietary hardware and software platform enables growers to monitor pond conditions, shrimp growth, and gather data for harvest prediction, disease alerts, and more. Additionally, Jala operates a marketplace to connect shrimp farmers to processing companies which allows farmers to become more competitive in the supply chain and increase transparency and product traceability. Today the platform is being used by more than 6,700 farms across Southeast Asia.

Jala intends to use the funds for expansion of the current business, developing its product roadmap, and exploring how they can contribute to sustainable certification standards for shrimp aquaculture.

Chris Wilson, partner at Kindrik Partners, says of the deal “We’re proud to have advised Jala on their recent round. Food sustainability and traceability are becoming increasingly important to today’s consumers and investors and there is a lot of room for innovation in the industry – we can’t wait to see how they grow.”

Read our other recent deal announcements here.

We’re pleased to have advised DiviGas, a Singapore-based startup cleaning up the hydrogen production industry, on their recent US$3.6 million seed round. The round was led by Energy Revolution Ventures and Mann + Hummel, a German industrial filter company. Entrepreneur First, Union Square Ventures, SOSV/HAX, Amasia VC, Volta Energy Technologies and Climate Capital also participated in the round.

DiviGas has engineered a product designed to efficiently separate and recover hydrogen and other gases at refineries and plants. Their innovative design allows customers to save money and minimise the wasteful and dangerous side-effects such as CO2 production and other mixed gases and chemicals.

The company was founded in 2019 by Dr. Ali Naderi, a researcher in the field of gas processing membranes, and Andre Lorenceau. The startup intends to use the funds to create a plant in Melbourne to produce the first industrial-scale pilots with select partners.

Chris Wilson, Partner at Kindrik Partners says, “we see DiviGas making a huge impact on sustainability efforts in the industrial energy sector – and there has never been a better time for it.”

Read our other recent deal announcements here.

We’re pleased to have advised Kilo, a Vietnam-based B2B e-commerce platform, on their recent $5 million pre-series A round. The round was led by Altos Ventures and January Capital. Other investors in the round included Goodwater Capital, Ascend Vietnam Ventures, Decisive Capital Management, Ratio Ventures and other angel investors.

Kilo connects wholesalers with micro, small and medium enterprises (MSMEs), providing more transparency and increased efficiency to the industry. The platform enables MSMEs to manage their inventory turnover and save costs. Owners can browse various suppliers and compare costs, as well as view in-stock availability for different items.

The company was founded in 2020 by Kartick Narayan, who is ex-Amazon and ex-Coupang. Today the company has thousands of MSMEs across 24 provinces in Vietnam.

The funds will allow Kilo to expand its team and focus on product development, such as adding features to its platform like financing, logistics, and self-service e-commerce store creation for MSMEs.

Chris Wilson, Partner at Kindrik Partners says, “we have seen significant interest in startups targeting MSMEs in developing countries across Southeast Asia. It is great to see technology companies like Kilo assisting these small businesses that are such a vital part of the market for consumers and the local economies.”

Read our other recent deal announcements here.

Our Southeast Asia team has advised Shoplinks, an Indonesian FMCG precision marketing platform, on its recent US$900,000 seed round. The round was led by Cocoon Capital and the Indonesian Women Empowerment Fund.

Shoplinks offers FMCG brands a marketing platform that distributes personalised coupons to shoppers through both online and offline channels in Indonesia. Founded in 2019 by serial entrepreneurs Teresa Condicion and JD Lee, the company aims to create a solution for brands that optimises their promotional budgets and reduces wasted budget from lack of personalisation of coupons to shoppers. In Indonesia, the lack of digitalisation in mom-and-pop stores and supermarkets often made it difficult for brands to effectively reach their customers, a situation that was compounded with the Covid-19 pandemic. Today, Shoplinks partners with brands such as Proctor & Gamble, Unilever, and Johnson & Johnson, processing thousands of coupon redemptions every month.

With its new round of funding, the company intends to increase its market presence in Indonesia before expanding into other Southeast Asian markets. The funds will also be used to grow its team and invest in product development.

Partner Lee Bagshaw says of the deal, “Indonesia’s online and offline retail opportunity is one of the largest in the world and is ripe for digital disruption. We look forward with interest at how Shoplinks will use their latest round of funding to accelerate digital transformation in the region.”

Read our other recent deal announcements here.

Our Southeast Asia team has advised Ackcio, a Singapore-based startup that builds wireless monitoring solutions for industrial monitoring, on its recent $4m series A round. The round was led by Atlas Ventures. Existing investors Wavemaker Partners, Aletra Capital Partners, and AccelerAsia Ventures, and new investors Enterprise Singapore and Seasight Holdings also participated in the round.

Founded in 2016 by Dr Nimantha Baranasuriya and Dr Mobashir Mohammad, Ackcio delivers wireless monitoring solutions to industries such as construction, infrastructure, rail, and mining. Ackcio’s technology helps contractors monitor projects remotely in real-time, increasing operational efficiency and improving worker safety.

In the past year, the company has expanded to 22 countries. The company intends to use this latest round to fund market expansion, scaling up its research and development efforts, and venturing into new industry verticals such as oil, gas, and energy.

Partner Chris Wilson says of the deal, “Ackcio has seen a tremendous amount of growth in a short amount of time, and with their latest injection of funding we look forward to seeing them continue to expand exponentially, both geographically and into new project verticals.”

Read our other recent deal announcements here.

We’re pleased to have advised Portcast, a Singapore-based logistics startup, on its recent US$3.2m pre-series A round. The round was led by Imperial Venture Fund, a joint corporate VC vehicle between Newtown Partners and South African logistics company Imperial. Other participants in the round include Wavemaker Partners, TMV, Innoport, and SGInnovate.

Portcast offers a SaaS platform that enables freight forwarders and manufacturers to achieve real-time visibility using historical data and AI modelling. It enables the logistics industry to track shipments in real time and to predict events that might affect their progress, such as tides, weather events, and pandemic-related supply issues. The platform can also map out the cascading effects of disruptions such as with the Suez Canal congestion.

Portcast was founded in 2018 by CEO and co-founder Nidhi Gupta. Prior to Portcast, Gupta spent 10 years in the logistics industry in senior leadership roles.

With its new round of funding, the company intends to double its team size, expand into new markets and launch new product features such as order-level visibility and scenario planning.

Partner Chris Wilson says of the deal, “Logistics is an industry that is ready for transformation, and this has become even more apparent in the context of the disruptions caused during the pandemic. We look forward to seeing Portcast’s technology making the logistics field more efficient, effective, and robust.”

Read our other recent deal announcements here.

We’re pleased to have advised Borneo, a Singapore-based data security platform, on their recent US$15.5m Series A round. The round was led by Vulcan Capital and existing investor Wavemaker Partners. Other participants in the round include Prosus Ventures and Lytical Ventures.

Borneo provides a suite of tools to identify sensitive and high-risk personal information through machine learning and APIs. These solutions integrate with existing tools and workflows and are targeted at technology firms that want to strengthen their privacy compliance.

The company was founded in 2020 by former Facebook and Uber exec Prithvi Rai. His elite team has tackled and solved privacy challenges at the likes of Facebook, Dropbox, Uber, and Yahoo!. The startup intends to use the funds to invest in its platform and to meet its rapidly growing customer demand.

Prithvi Rai, CEO & Founder of Borneo says, “Borneo is fast becoming the guardrails for the new data economy. We can prevent data leaks and privacy violations that can result in multi-million dollar fines and erode end-user trust.”

Chris Wilson, Partner at Kindrik Partners says, “It is always exciting to working with a accomplished founder like Prithvi, especially in an area like personal privacy which is of such critical importance to modern businesses.”

Read our other recent deal announcements here.

We’re pleased to have advised Ai Palette, a foodtech startup that uses machine learning to spot food trends, on their recent US$4.4m Series A round. The oversubscribed round was co-led by pi Ventures and Exfinity Venture Partners. AgFunder, Decacorn Capital, and Anthill Ventures also participated in the round.

Ai Palette uses machine learning and AI to help CPG (consumer packaged goods) companies predict consumer trends and speed up the R&D process. Its product, Foresight Engine, aggregates data from various different sources such as social media, search engines, blogs, recipes, images, menus and company data, and can recognise and analyse comments in 15 different languages.

The company was founded in 2018 by Somsubhra GanChoudhuri and Himanshu Upreti, who met through venture builder Entrepreneur First. The company is based in Singapore, with an engineering hub in Bangalore and plans to use the funds to expand its customer base beyond Asia, recruit new talent in data science and engineering, and develop new product lines.

“Ai Palette is bringing some great innovation in the food space to the table with their product” (no pun intended), partner Chris Wilson says of the deal. “Their oversubscribed Series A shows the confidence that investors have in the technology and the opportunity ahead of them.”

Read our other recent deal announcements here.

Our Southeast Asia team has advised Lifepal, a digital direct-to-consumer (D2C) insurance marketplace, on its US$9m series A funding round. The oversubscribed round was led by ProBatus Capital. Cathay Innovation, Insignia Ventures Partners, ATM Capital and Hustle Fund also participated in the round.

Lifepal was founded in 2019 by former Lazada execs Giacomo Ficari, Nicolo Robba as well as tech veterans Benny Fajarai and Reza Muhammad. Lifepal’s insurance marketplace is the largest of its kind in Indonesia, and receives four million visitors to its platform monthly. Visitors can access over 300 different policies that cover different areas such as health, life, automotive, property, and travel. Visitors can also access educational content that helps them understand and articulate their needs, and then the platform allows them to compare up to 50 different providers to find the policy that best suits them.

The company intends to put the funding towards product development and customer experience.

“Startups in the insurance and fintech space are getting a lot of attention in Southeast Asia as innovative companies like Lifepal are finding ways to connect with individuals in markets that have traditionally been unbanked or underserved”, partner Chris Wilson says of the deal. “With customer behaviour increasingly shifting to digital services in Indonesia, the team has a huge opportunity in front of them.”

Read our other recent deal announcements here.

Our Southeast Asia team have advised ADPList, a cross-border mentoring platform, on their recent US$1.3m seed round. The round was led by Surge, the accelerator programme run by Sequoia Capital India. The funding is supported by prominent angel investors Crystal Widjaja (ex-Gojek executive), JJ Chai (CEO of Rainforest), Quek Siu Rui (Co-founder & CEO, Carousell), Ting Feng Toh (Co-founder of GetGo), and Zopim Founders (Royston Tay, Wen Xiang Wu, and Yang Bin Kwok).

ADPList (formerly ‘Amazing Design People List’) connects people in the design and product management community to mentors in some of the most popular tech companies in the world such as Facebook, Amazon, Apple, Netflix, and Google. Mentors can show their availability on a shared calendar that mentees can access in order to schedule virtual sessions. Virtual sessions are conducted within the platform via one-on-one video calls, small group mentoring, and townhall-style talks.

ADPList, originally conceived as a publicly shared Google spreadsheet, started out in April 2020 by Felix Lee and James Baduor as a way for designers to provide peer support and share advice with others impacted by the pandemic. Today, it is available in over 70 countries with 20,500 mentees, more than 2,500 mentors, and 5,000 booked sessions a month. Booking a mentor at ADPList is currently free, with plans to commercialise the service as well as expand the platform to include other professions.

“It’s warming to see people wanting to give back and support upcoming talent in their industry”, partner Chris Wilson says of the deal. “The cross-border element also allows knowledge from some of the most successful companies in the world to circulate beyond Silicon Valley, which is promising for the development of other tech hubs.”

Read our other recent deal announcements here.

Kindrik Partners recently advised Shikho, an edtech startup focused on making education accessible and affordable for Bangladeshi students, on its $1.3million seed funding round.

LearnStart, the seed fund of Silicon Valley-based edtech investment fund Learn Capital, and Anchorless Bangladesh, a New York-based early-stage venture capital firm, led the round. It also had participation from Wavemaker and Ankgur Nagpal, founder and CEO of online platform Teachable. The company previously raised $275,000 in pre-seed financing from LearnStart and other angel investors.

The content on the Shikho platform is based on the Bangladeshi National Curriculum and features animated video lessons, interactive live classes, and continuous assessment. It also includes gamification techniques such as point-scoring systems and leaderboards, where students can measure their performance against users at their school, or across the entire app.

The company was founded in April 2019 by CEO Shahir Chowdhury and COO Zeeshan Zakaria. The pair previously worked in finance but both have connections to the education sector – both Chowdhury’s parents were teachers, and Zakaria pivoted from finance to teaching mathematics.

Shikho plans to use the funds to continue hiring edtech talent and accelerating content and technology development, in addition to focusing on user acquisition, including offline sales teams for school wide presence.

Partner Lee Bagshaw says of the deal, “the market opportunity for Shikho is massive and they’re poised to take the lead in remote learning in Bangladesh and beyond – it was a pleasure to work with them on this deal.”

Read our other recent deal announcements here.

We’re pleased to have advised Edamama, an e-commerce platform targeted at mothers in the Philippines, on its recent US$5 million pre-series A round. Gentree Fund, Robinsons Retail Holdings, Kickstart Ventures, Foxmont Capital partners, and other angel investors participated in the round.

Edamama was launched in mid 2020 by Nishant and Bela Gupta D’Souza and grew substantially during the pandemic as customer purchasing shifted from brick-and-mortar stores to online. In addition to purchasing items online, customers can create personalised wish lists with Edamama’s Gift Registry that can be shared with friends and family. The startup also offers Explore, a platform where parents can book child-related classes and activities, and Subscribe & Save, the Philippines’ first online diaper subscription service.

The startup intends to use the funds raised to develop new platform features, enhance its range of trusted products and services, and expand its warehouse and delivery capabilities.

Co-Founder Nishant D’Souza commented, “We’re very proud to bring on board these eminent strategic investors being such an early stage venture – the recognition of our business momentum in an unprecedented operating environment is a real achievement for our team.”

Lee Bagshaw says of the deal, “The last year or so has for obvious reasons seen a huge rise in e-commerce activity, and it’s been great to see Edamama leverage this – we look forward to seeing what they do next.”

Read our other recent deal announcements here.

Our guide covers venture debt for startups and fast-growing tech companies in Southeast Asia – what it is, the different forms of venture debt, why to use it compared to bank debt or equity financing, when best to use it, and key terms to consider when negotiating with lenders.

Have questions about the venture debt process? Feel free to get in touch with us.

Access the guide by filling out your details below:

Our Southeast Asia team have advised Singapore-based startup impress.ai on its recent pre-series A round. The round was led by Summit 29K with Seeds Capital, the investment arm of Enterprise Singapore, also participating.

impress.ai was founded in 2017 by Sudhanshu Ahuja, Vaisagh Viswanathan and Amrith Dhananjayan. The startup has developed an AI chatbot for recruiters and hiring managers that allows those users to interview, engage, and shortlist candidates and help them at every stage of the talent acquisition process. The product is already being used enterprise clients such as Accenture, DBS, and Singtel.

The latest round of funding will be used to accelerate product development, accelerate hiring, and expand to Australia, Hong Kong, and Taiwan.

Read our other recent deal announcements here.

Our Southeast Asia team have advised e-commerce aggregator Rainforest on its recently completed seed funding round. The round was led by Nordstar with Insignia Ventures Partners also participating. The round includes $6.5 million in equity financing and a $30 million venture debt component from an undisclosed American debt fund.

Rainforest was founded in January 2021 by JJ Chai, Jason Tan and Per-Ola Röst. The founders are alumni of some of Southeast Asia’s top startups including Carousell and Fave (who have also been our clients).

Rainforest acquires direct to consumer (DTC) e-commerce brands who sell through Amazon marketplace. It is focused on ‘rolling up’ APAC-based microbrands and has acquired three brands so far. The funding will be used to add more brands sold through Amazon’s B2B service Fulfilled By Amazon (FBA) to Rainforest’s portfolio.

Partner Lee Bagshaw says of the deal, “It was a pleasure to help Rainforest with their seed funding round. The team’s previous experience in rapidly scaling digital companies is second to none and we look forward to seeing Rainforest’s progress having raised sizable funding.”

Read our other recent deal announcements here.

We’re delighted to have advised Fave, the Malaysia-based fintech platform providing QR payments and loyalty cashback to restaurants and retailers, on its acquisition by Pine Labs, the Indian Sequoia-backed payment and merchants platform.

The deal is valued at more than US$45 million. Pine Labs intends to roll out the Fave payments app in India across a network of 500,000 merchants on its platform.

As part of the deal, Fave’s founders Joel Neoh and Yeoh Chen Chow will continue to lead the consumer platform for the group across Asia. There are also plans to hire over 100 new employees across both Southeast Asia and India.

Fave started out in 2015 as fitness sharing platform KFit before stepping into multi-category local commerce with the launch of Fave.

As Fave took on speed, Kindrik advised the business on several funding rounds as well as its acquisitions of Groupon’s businesses in Indonesia, Malaysia and Singapore in 2016 and 2017.

In 2020, Fave entered into a strategic partnership with Pine Labs where Fave’s QR code was integrated with Pine Lab’s terminals, enabling an integrated platform for acceptance and loyalty cashback solutions.

Fave co-founder Chen Chow Yeoh says “Lee Bagshaw and Kindrik worked with us through all our funding rounds, our acquisition of Groupon companies and now our exit. We’re thankful for their expertise and guidance in the VC and tech M&A space.”

Partner Lee Bagshaw says, “It’s been a six year journey working with Joel and Chen Chow starting when the business was trading as KFit. We’re pleased to have watched Fave grow and play a role of the digital transformation of payments across Southeast Asia. We wish them the best of luck on their continued journey with Pine Labs.”

In the last few years, convertible notes have been frequently used on Singapore financings. Perhaps less common has been the use of SAFEs – the instrument created by Y-Combinator (YC) several years ago. However SAFEs are on the increase on fundraising deals across Southeast Asia.

Two years ago, YC reinvented the SAFE and launched what is now known as the ‘post-money’ SAFE. And just last month they released beta versions of the “Valuation Cap, no Discount” post-money safe and side letter specifically for companies registered in Singapore. You can access these here.

quick reminder – what’s a SAFE?

A simple agreement for future equity – in short, it’s an instrument convertible into shares similar to a KISS or convertible note. What’s different with a SAFE is that it doesn’t typically have any interest accruing, nor any maturity date and repayment obligation. They are therefore seen as a founder friendly investment tool to raise capital.

Like KISSes and other convertible notes, SAFEs typically convert into shares on the basis of a conversion price which is usually an agreed discount to the price of the next equity round, but which is subject to an overall valuation cap – i.e. whichever gives the lower price for investors.

so, what changed with the ‘post-money’ SAFE?

post-money SAFEs don’t dilute each other (bad news for founders)

The main change is that the new SAFE uses a post-money valuation cap instead of pre-money. The drafting change is fairly subtle to see: the definition of Fully Diluted Capital in the SAFE is amended to reflect the new principle. However, the impact can be significant. It means that the company’s valuation for calculating the conversion is “post” (i.e. after) the conversion of any other SAFEs or convertible instruments issued by the company, but prior to the valuation of the company immediately after the equity financing round. This results in further dilution for founders on conversion and potentially to any other investors that do not hold post-money SAFEs.

Just to be clear and to dispel a myth, by ‘post-money’, this is post all other SAFEs and convertible notes, but not post the next equity financing as well, as some founders have asked. That really would cause dilution!

Under post-money SAFEs, the post-equity financing option pool is no longer factored into the pre-money calculations, which actually benefits founders from a dilution perspective. Under the original SAFE, option pool expansions resulted in SAFE investors receiving additional shares. However, overall this doesn’t balance out the additional dilutive effect outlined above.

you’ll only feel the impact with multiple rounds of SAFEs

It is worth pointing out that for a company that only ever raises one SAFE investment round, a post-money SAFE has no real impact. Rather, it comes into play when more than one series of SAFEs or other convertible notes are issued. In Singapore, we perhaps see this less commonly than say in the US where substantial amounts are often invested using SAFEs and other convertible instruments, and not only in the first round of investment.

easier to calculate cap table (good news for founders)

YC’s view at the time of launching the new SAFE was that it makes the maths simpler for everyone and creates more certainty over ownership and dilution. Which is probably true. But if you issue more than one round of SAFEs or other convertible notes, and you use post-money SAFEs, founders will likely experience more dilution on conversion than they would have done under the original YC SAFE, simple as that.

In light of this, if presented with a post-money SAFE, founders may want to negotiate up the valuation cap to mitigate against the dilutive impacts potentially coming into effect.

what else did YC change?

The original YC SAFE granted holders a pro-rata right on the next financing round. The new SAFE doesn’t automatically include this. Instead, YC put out a separate side letter on their website under which these additional pro-rata rights might be granted.

Also, the old SAFE could only ever be amended by the holder. The new SAFE on the other hand permits amendments by written consent from a majority of SAFE holders. This is something we think is valuable on all convertible instruments, i.e. the holders effectively make decisions on a consensus basis, avoiding one single small investor taking a different view holding things up.

other key points to remember about a SAFE

Not specific to the new post money version, but whenever drafting or reviewing a SAFE, keep these tips in mind:

- Look out for most favoured nation (MFN) provisions. These enable early investors to have the benefit of any rights granted to future SAFE holders which might be more beneficial. If nothing else, it can be a burden reissuing new SAFEs on these better terms to lots of prior investors.

- SAFEs typically convert automatically on completion of the next equity financing. There should ideally be no minimum amount to be raised to trigger this automatic conversion under a SAFE. Some investors like to include a threshold to ensure it is a legitimate fundraising round. Always be careful you do not go too high with this so as to prevent automatic conversion of the SAFE.

- A SAFE (like all convertible instruments) should include language to the effect that, on conversion, holders will only have the benefit of their lower conversion price for the purposes of liquidation preference and anti-dilution rights. This can be achieved through issuing a separate class of “shadow” preferred shares, or just by drafting carefully the relevant provisions in the constitution and shareholders agreement put in place on the equity round.

round up

If you are presented with any kind of SAFE right now, it will most likely be the post-money version, so come and have a chat to us.

Our Southeast Asia team have advised greentech startup Green Li-ion on its US$3.45m seed funding round. The round was led by US-based cleantech company LiNiCo Corporation. Previously, Green Li-ion raised US$400,000 in pre-seed funding as part of Entrepreneur First’s 2020 cohort in Singapore.

Green Li-ion produces sustainable solutions for battery rejuvenation and recycling.

“The precious metals used to manufacture lithium-ion batteries are often mined in socially and environmentally damaging ways and the reason why they are not recycled is that it is simply not economical to do so with the current technology,” says Leon Farrant, Green Li-ion’s Chief Executive Officer.

“With Green Li-ion, we are committed to introducing the next generation of battery rejuvenation and closing the loop,” says Leon.

The company intends to put the funding towards hardware development, including engineering and specialist manufacturing support.

On the topic of the capital raise, Leon says, “There were a number of moving parts to the transaction and Kindrik were invaluable in getting the deal over the line.”

“It’s great to see greentech get funded here in Singapore and see Green Li-ion leading the charge in sustainable battery recycling”, partner Chris Wilson says.

“It was a pleasure helping them with their seed funding round and we can’t wait to see what they do next.”

From capital raisings to drafting governance contracts, we help startups every day with their legal needs. We’ve created a new guide to help founders find their feet: Top Ten Legal Templates for Startups: A guide for companies based in Southeast Asia.

This guide contains basic tips when putting this paperwork in place. Having these documents in order can help your startup further down the line, particularly when raising investment. With each template, we cover what it does, when a startup might need to use it, and essential points that founders should wrap their heads around.

All legal agreements we cover in the guide are also available for download free on our website. These templates include explanatory notes to help founders and non-lawyers complete the agreement.

Have questions about our guide or one of the templates? Feel free to get in touch with us if you’d like some help adapting one of the agreements we’ve recommended.

Access the guide by filling out your details below:

When writing this time last year, we were full of optimism for 2020. A lesson in not looking too far ahead!

reflections on the region

Unsurprisingly in such an extraordinarily difficult year, it’s been tough for many of our tech clients across Southeast Asia. Some have hunkered down to conserve cash, some raised emergency financing, and others have had to pivot temporarily or permanently. For those more fortunate, it was business as usual.

Fortunately, our deal flow in 2020 has remained strong and kept us busy. Globally, the number and size of technology M&A and investment transactions has amazed observers, including ourselves. Regionally, Southeast Asia continues to be extremely attractive to both local and global investors. As Techcrunch very recently noted, Singapore has firmly put its flag down as “Asia’s Silicon Valley”. Additionally, Singapore and Vietnam, along with much of Asia, have coped with the pandemic much better than the US and Europe. As a result we expect investor appetite for these young digital economies to continue increasing rapidly, both in terms of setting up shop and seeking investment opportunities. This suggests a busy time for the SEA tech and venture focused law firms such as Kindrik as we head into 2021.

firm highlights

This year, there was no exhibiting for us at Echelon or Tech in Asia. Our regular speaking events hosted by accelerators and incubators across the region also went exclusively online. Indeed, as regional accelerator programmes in the main paused for the year, there was a drop off in the flow of new startups emerging and raising seed capital. However, 2020 still saw plenty of activity for the team. Deals occasionally took slightly longer to close, but investor-friendly VC terms and down rounds didn’t materialise for the most part. All in all, it was business as usual on fundraising transactions. There were more bridge financings and more convertible debt than usual as investors looked to support existing portfolio companies over the difficult months.

In terms of other highlights:

- we renamed ourselves Kindrik Partners to take us forward with a dynamic brand

- we acted for VC funds on over 10 Series A or later financing transactions

- we advised on many notable financing deals including:

- Fave on its transformative partnership with Pine Labs

- Neat, the Hong Kong based fintech startup, on a US$11 million series A

- Silent Eight, the regtech startup leveraging artificial intelligence, on its latest funding round, bringing the company’s total capital raised to US$15 million.

- See-Mode Technologies on its series A funding led by Mass Mutual Ventures.

- Singapore-based Horizon Quantum Computing on its financing round led by Sequoia.

looking ahead

We’d expect 2021 to see some consolidation in the startup ecosystem and potentially some small (and maybe larger) M&A deals. Who knows, we may even see the biggest merger of all between Grab and Go-Jek. Those tech companies who raised in 2019, and have kept their heads down this year, will probably come up for air and engage with the investor community. We also expect a lot of the VCs who kept some of their powder dry in 2020 to be particularly active in the first half of 2021. Indeed, our pipeline already looks good.

Thanks to the Kindrik Singapore team who have been working at home for the best part of the year – you’ve done a great job. Best wishes too to all our clients in Asia for 2021. It can only get better.

We’re pleased to have advised Singapore-based venture capital firm, Monk’s Hill Ventures (MHV), on two recent series A financings.

Most recently, Indonesian logistics platform Logisly announced their US$6million series A financing led by MHV. The Jakarta-based startup provides B2B tech-enabled logistics solutions.

This follows on from Malaysian-based startup, Go-Get, completing their series A investment in October, again led by MHV. The on-demand platform currently has over 20,000 gig workers, and has onboarded 5,000 businesses of all sizes, from micro SMEs to MNCs.

Partner, Lee Bagshaw says: “Whilst the global startup economy battles with COVID-19, it is encouraging to see continuing investment activity across Southeast Asia, with VC transactions led by notable investors like Monk’s Hill Ventures. For platforms enabling disruptive areas such as on-demand and logistics, the region remains very attractive for investors.”

Our Southeast Asia team have advised Philippines-based fintech company JazzyPay on its seed funding round led by early-stage venture capital firm Cocoon Capital.

JazzyPay allows its partners to accept payment via 27 payment methods, including credit and debit cards, online banking, e-wallets and over-the-counter deposits. The company was launched in 2018 and has been serving merchants that typically have only accepted cash and cheque payments, including organisations such as hospitals, schools, clinics and medical suppliers.

“In an emergency, the payment method should be the least of your worries,” JazzyPay Chief Operating Officer and co-founder Kathleen Acosta said.

The company intends to put the funding towards product development as well as expanding its network of partner merchants.

Senior solicitor Sarah Yen says of the deal, “It was a pleasure to help JazzyPay with their capital raise – they are solving a real need for Filipinos and we look forward to seeing their continued growth.”

We recently helped Neat, a Hong Kong based fintech startup, on a US$4 million extension to their US$11 million Series A round which closed earlier this year.

Neat started over two years ago with a focus on making business accounts accessible to startups and SMEs in Hong Kong. Existing investors that participated in the series A extension include Mass Mutual Vetnures, Linear Capital, Pacific Century Group, and Robby Hilkowitz, as well as new investor Vectr Fintech.

The coronavirus pandemic has not stopped Neat’s momentum.

“Some of the world’s most successful companies were born during or just after the financial crisis of 2008, think of WhatsApp and Uber,” says David Rosa, CEO.

“The majority of businesses founded during COVID-19 will have a digital-first mindset, which means they will have an opportunity to start trading globally from day one. We’re excited to be supporting this new wave of international entrepreneurs.”

With the new funding, Neat will continue product development as well as improving its customer support experience and fuelling its growth.

Our capital raising lawyers in Singapore have had a busy first half of 2020, even as Covid-19 impacts globally on fundraising. As at end of July, we had 42 fundraisings by Southeast Asian companies, slightly above where we were at the same point last year.

Our numbers (compared with previous years) implies that startup financing, particularly in Asia, has remained pretty resilient. The availability of capital in Southeast Asia, with the particularly vibrant VC scene in Singapore, has ensured financings have ticked over during lockdowns.

It is fair to say that we have seen more bridge financings amongst existing clients than normal, compared to fundraising for new companies. As investors look to support existing portfolio companies over the next few difficult months, many companies have had to change their investment strategy. Venture debt may play an increased role alongside traditional equity financing in more deals we see going forward. Thankfully, to date, we’ve not seen many down rounds, but these could increase over the next 12 months unless founders can find alternative financing structures.

There’s a lot of discussion in the market about how the pandemic has changed the investment landscape, with deals being pulled or delayed. Fortunately, we’ve not seen too much evidence of that in the tech space so far. Deals are taking slightly longer however, and we expect more investor friendly terms to appear.

Stay tuned – we’ll be keeping a close watch to see how fundraisings in tech companies in our key markets continue to look over the rest of 2020.

Our Southeast Asia team have advised See-Mode Technologies on its recently completed series A funding round. The round was led by Mass Mutual Ventures Southeast Asia. Other investors in the round include existing investors Blackbird Ventures, Cocoon Capital, Entrepreneur First, and SGInnovate.

See-Mode Technologies was founded in 2017 by Dr Mohammadzadeh and Dr Sadaf Monajemi. See-Mode uses artificial intelligence to help better predict the risk of stroke and vascular diseases.

The funding will be used to increase its headcount, expand its research and development (R&D) and engineering capabilities, and expand the business into Europe and the United States.

Partner Chris Wilson says of the deal, “It was a pleasure to help See-Mode with their series A funding round. Their mission of empowering clinicians to prevent stroke is admirable and we are excited to watch their continued growth.”

Read our other recent deal announcements here.