BLOG

evolving VC terms in southeast asia

share:

No one’s talking about venture capital anymore – that boring old-fashioned way of raising money. With ICOs a threat to venture itself, you might think that VCs are going easier on companies. Not so, from our experience. Approaching the end of 2017, we reflect on the evolving deal terms in Southeast Asia.

deals taking longer

From term sheet to closing, transactions are taking longer. VCs are no longer investing at a rapid pace and can take more time on deals. For founders, that means extra due diligence and investors less inclined to negotiate. Southeast Asia has lots of first-time funds and corporate VCs and these types of investors sometimes can be more risk adverse. Investors are also reviewing transaction documents from earlier deals as part of liquidity events or restructures. Inevitably they seek to address any weaknesses of the terms of those documents going forward. The end result can be tougher terms for founders on their new investment deals.

convergence of terms

We’re still not close to having any standardised documents in the region, but investment documents do the rounds and investors adopt terms from each other’s deals. Whilst standardisation can be good news for founders in terms of streamlining the negotiation process, it also means you’ll hear the inevitable sound of investors claiming that a position which is favourable to them is now market standard.

de-risking the deal

Specifically, with exit and redemption rights. These terms set the clock running for the company and require an exit or other buy-out of the investors after a set period of time. A couple of years ago, we only saw these occasionally. Now VCs are asking for such rights on series A or even pre-series rounds on a regular basis. We have also seen exit periods as short as 5 years (with 7 years being more standard).

board control

We’re occasionally seeing company boards set up so that founders effectively lose their majority, even at an early stage. There may be more than one investor director appointed, or perhaps an independent director. This means, aside from the usual investor veto rights, founders are not even in control of the day-to-day running of the business at board level. Fortunately, this is a relatively rare scenario.

tips for founders

Negotiating is hard work given the imbalance between the folks with the money and those asking for it. How should founders respond to these trends? Think about the following:

- Reject the market standard argument. Most issues should be up for discussion (subject to point 2 below). The VC should have to justify their positions logically, rather than relying on a broad statement that something is apparently market standard.

- Know your investor. Do your due diligence on the investor (including asking your lawyer about them). That way you’ll know what’s coming down the track from the outset. If a particular VC requires a certain term on all of its deals, then you will need to be a pretty special prospect to negotiate it away.

- Negotiate at term sheet stage. Investors expect the final documents to align with the provisions of the signed term sheet. Avoid presenting a signed term sheet to your lawyer and asking him or her to get you the best outcome on the deal. They’ll do their best, but the horse has already bolted by that point unfortunately.

- Take governance seriously. When you raise multiple rounds, control of the company can quickly be lost with investors at each funding stage looking for a seat at the board table. Focus on retaining key decision-making power for the founders at board level, even if investor directors can participate in discussions. This should of course align with the best interests of your investors.

If you would like to have a chat about raising capital and negotiating VC transaction documents in Southeast Asia, drop an email to Lee or Chris.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

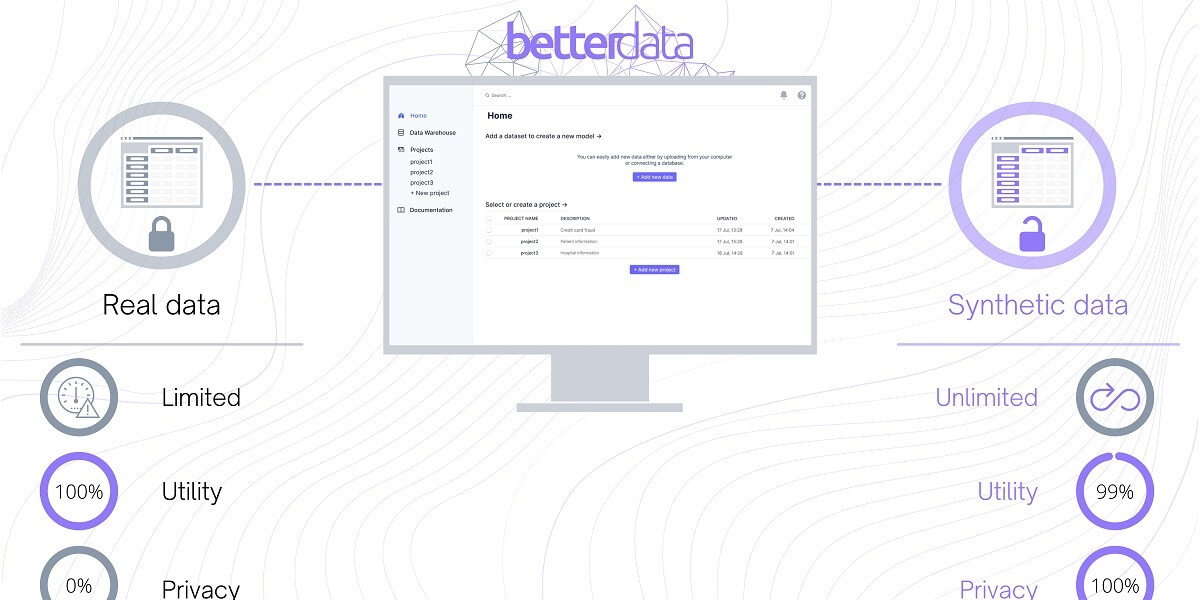

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.