BLOG

bridge financing for startups in an economic crisis

share:

Startups generally die because they run out cash, not ideas. At this time, founders will be looking closely at their cash and runway. As VCs hunker down, new capital will be scarcer and startups may have to scramble for cash using bridge financings with less founder friendly terms.

We’ve considered some of the issues around startups structuring bridge financing transactions in an economic crisis – using both equity or convertible notes. Here’s our rundown of what we think founders might face.

(You can view our other Covid-19 related content on our blog.)

priced equity rounds

- Valuation – The main issue here is low valuations. Startups will want to avoid a down round at all costs which may significantly dilute existing shareholders. That might mean we see more debt instruments like convertible notes which don’t fix a valuation immediately (we discuss convertible notes below).

- Tranched investments – Investors may increasingly look to tranched investments (being investments where the funds are made available in stages, instead of the total investment amount being made available upfront). Founders will need to consider how much risk this introduces to the prospect of actually seeing the money. Are the tranches subject to KPIs? If so, are the KPIs achievable and able to be measured objectively, so you don’t end up in a dispute with investors about whether or not a KPI has been satisfied? The conditions to closing of any deferred investment amounts will also need to be reviewed carefully. Is there any material adverse event (MAE) clause triggered by a deterioration in the financial performance of the business? If so, you may need to be clear on what is material in these extraordinary economic circumstances, where clearly the goal posts have shifted.

- Secondaries – Startups may need to structure deals with a mix of primary offers (new investment monies) and secondaries (sales of shares by existing shareholders) – with secondaries at a discounted price. This will enable some VCs, angels and other early investors to exit and cash out. Founders may need to think about offering this to sweeten deals for existing investors.

- Term sheets – These are non-binding. Investors do not typically sign term sheets and then withdraw for market reasons. But we’re in extraordinary times. Investors can in theory walk away without any reason. Keep exclusivity periods in term sheets to a minimum (e.g. not more than 30 days) so if an investor does start to look like it is having a rethink, the company can quickly move on to other investment opportunities.

- Deal process – Startups need deals to close quickly. The opposite is likely to happen however, as investors take time to consider how the business will look on the other side of COVID-19’s impacts. Founders should consider limiting the number of new investors and engage early with existing shareholders on any terms which impact them. The simpler the transaction and the fewer the surprises for existing shareholders, the faster the equity deal is likely to close.

convertible notes

- Increase in debt – There will inevitably be more debt financings during the remainder of 2020 and beyond. Mainly as debt holders take priority over shareholders in a winding up, and investors will prefer this position. In the startup world that most likely means convertible notes rather than traditional bank debt (which won’t be available anyway), and venture debt (which usually supplements equity financing rounds).

- Type of instrument – We’d expect investors to insist on conventional convertible notes (or a KISS) for the time being, as opposed to SAFEs. This is because they include a maturity date – the date on which the debt must be repaid if the company hasn’t closed the next equity financing round – which partially de-risks the investment for investors. Typically maturity periods have been 18-24 months. In normal times, this would be more than sufficient time to close the next equity financing. This may no longer be the case, particularly if the VC industry shuts down for a period. Startups will need to consider the risks of taking on debt, repayable with interest on a future maturity date, if they can’t close the next equity round. If, as a startup, you don’t honestly believe you’ll be able to close the next equity round before you’re required to repay convertible debt and interest, you’d be better off raising an equity round instead of entering into a convertible note, even if it means undertaking a dreaded down round.

- Terms – One advantage of using convertible notes over equity is usually speed. Without lots of warranties and other covenants to negotiate, traditionally startups are more likely to close convertible note deals quicker. However, convertible notes in bridge financing scenarios, which often occur post a seed round or even after series A or B have occurred, can include much more investor friendly terms, including broadly drafted events of default, long form reps and warranties, and even new governance provisions. Founders will need to consider whether it still makes sense for the business to take on debt if they end up negotiating the same type of issues they would on an equity deal.

- Security – Typically convertible notes have been unsecured. We think it is highly unlikely that we’ll see secured bridge financings, certainly not with traditional VCs. But, this is a new world, and who knows how angels or other investors might look at things.

- Warrants – We’re expecting the use of warrants to increase alongside convertible notes. Warrants allow for further shares to be issued in the future at the option of the investors. This de-risks the transaction for investors but gives them the option to double down in the future at the same conversion price if the business is successful at riding out the impacts of Covid-19.

If you are raising capital or have a transaction where existing shareholders are selling down, you can book a 30-minute free consultation with one of our startup lawyers to discuss. Pick a time that suits you via our online booking tool.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

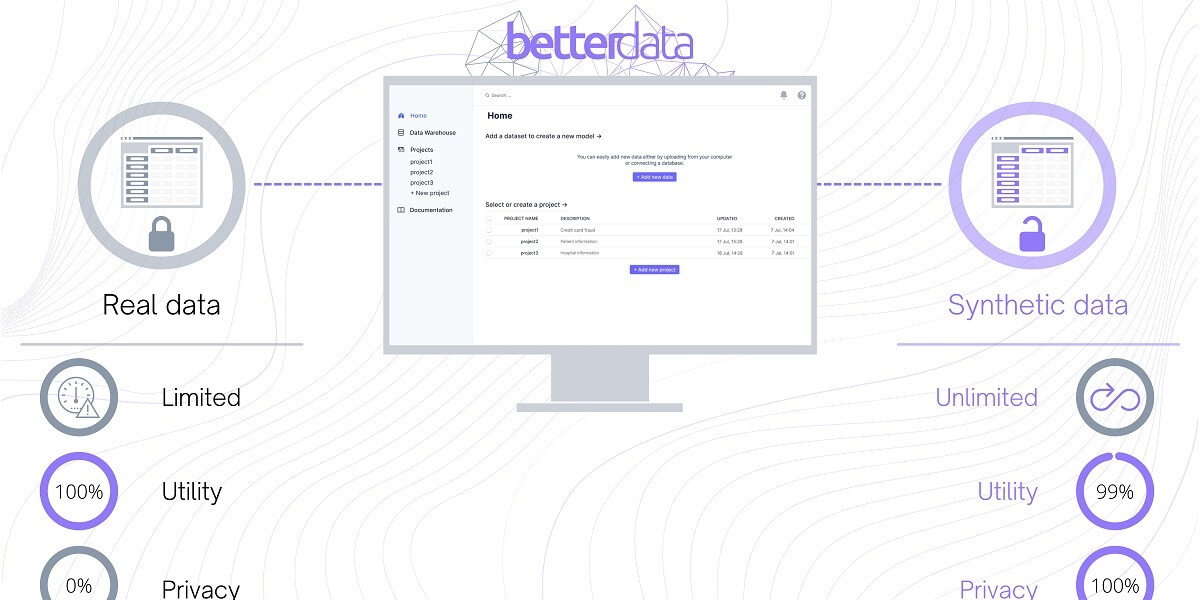

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.