BLOG

post-money convertible notes

share:

Back in 2018, Y-Combinator (YC) updated their core investment instrument and launched what is now known as the post-money SAFE.

We analysed the post-money SAFE back in 2020 – see our blog here https://kindrik.co.nz/blogs/a-primer-on-post-money-safes-in-new-zealand/. The main difference between a pre-money and post-money SAFE is that, on conversion, under the pre-money terms the calculation of the number of conversion shares does not include the conversion of the SAFE itself and any other convertible instruments in issue (other convertible securities). With a post-money SAFE all of these other convertible securities are included. The end result is further dilution for existing ordinary shareholders on conversion of the post-money SAFE.

But what about convertible notes? Have they remained drafted on a pre-money basis or, like the SAFE, has the market moved towards the more investor friendly post-money position?

Convertible notes v SAFEs

The terms of convertibles notes differ from SAFEs. SAFEs remain outstanding until a conversion event occurs, or the company has a liquidity event. So, in effect, there is no repayment obligation. In contrast, convertible notes have a maturity date and generally accrue interest. Therefore, startups have no time pressure to close an equity financing under a SAFE. Whereas under a convertible note, they might need to get it done within say 18 months, or the note could be repayable. For that reason, SAFEs are generally the preferred document for founders.

The market has certainly followed YC’s lead when it comes to SAFEs. Most SAFEs we now see are the post-money version. However, the same can’t be said for convertible notes, for which conversion into shares is still calculated on the more founder friendly pre-money calculation. Looking at templates available online, whether provided by law firms (including our own!), VCs or industry bodies, this looks to be the consistent approach across the board. That said, we do occasionally see them on deals where investors are looking to secure a better position or when they simply draft the document incorrectly.

Round up

Founders should be cautious here and take advice at the term sheet stage so there is no ambiguity when everyone comes to drafting the final instrument. If any post-money instrument is used, it may require founders to rethink the valuation cap on the deal.

Investors could argue that there is nothing intrinsically different between a SAFE and a convertible note in terms of how equity should be calculated on a conversion event. I.e. why shouldn’t the number of shares be determined on the same basis for each?

However, YC’s justification at the time of launching the new SAFE was that it makes the conversion calculation simpler and creates more certainty over the future dilution. Which is certainly true. But YC’s model is about speed and efficiency and they invest in multiple companies in their intakes. A SAFE is also a pretty founder friendly investment instrument, and rarely negotiated much. A convertible note, on the other hand, has other disadvantages to founders and more onerous terms, in particular, interest and repayment obligations. Notes also tend to include information rights, a most favoured nation clause, events of default provisions and other covenants that don’t typically appear in SAFEs.

Taking that into consideration, our view remains that convertible notes should be drafted on a pre-money basis, and that post-money notes remain non-market.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

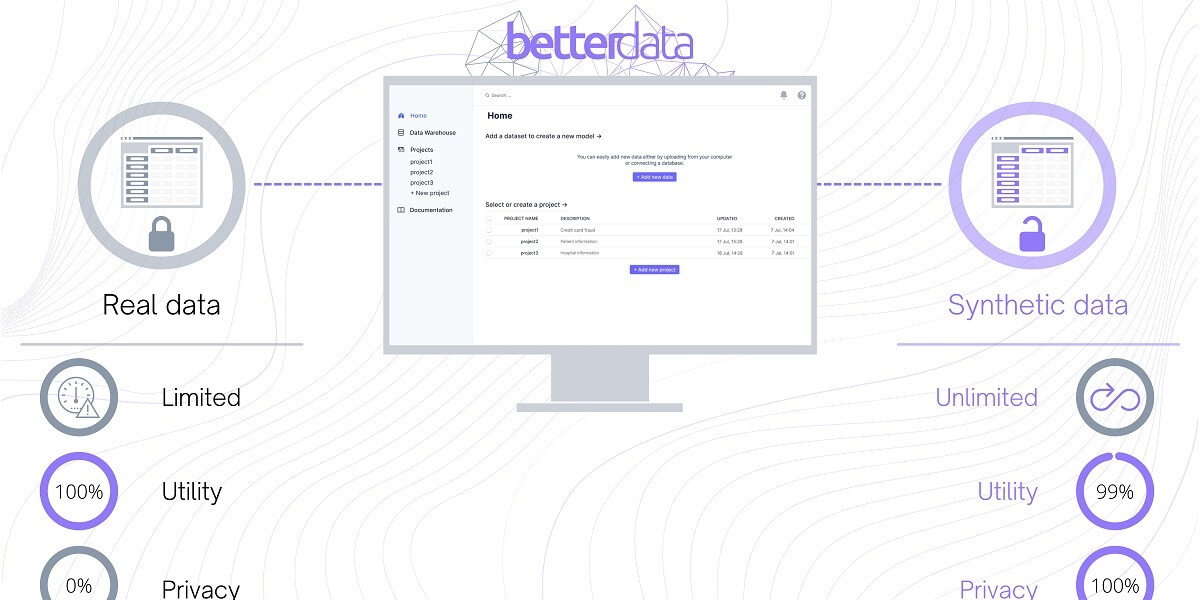

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.