BLOG

new singapore model VC documents

share:

The Singapore Academy of Law (SAL) and Singapore Venture Capital and Private Equity Association (SVCA) have collaborated to create industry standard documents for VC investments in Singapore. These Venture Capital Investment Model Agreements (VIMA) are available here and are for use on pre-series A and series A transactions.

The documents released are as follows:

- Venture Capital Lexicon

- Non-Disclosure Agreement

- Convertible Agreement Regarding Equity (CARE)

- Term sheet

- Short Form Term Sheet

- Subscription Agreement

- Shareholders’ Agreement

Here are our thoughts on the new financing documents.

convertible agreement regarding equity (CARE)

First we had the SAFE, then the KISS, and now we have the CARE. The CARE is based on the principles of a SAFE (rather than a KISS). Specifically, the CARE has a Maturity Date but no repayment obligation, i.e. on the Maturity Date the investor can elect to convert at a Maturity Cap (value to be agreed) or leave the investment amount outstanding, repayable only on a dissolution event. The CARE also has no interest component.

Our experience is that SAFEs are less common than KISS notes in Southeast Asia. Investors usually want the option to either convert their investment amount to shares or require repayment in cash on maturity. This puts some time pressure on founders to deliver an equity financing transaction. If the CARE template becomes the market standard it would represent a win for founders. However, investors might respond by offering discounted Maturity Caps (whereas in a typical KISS the maturity valuation is usually the same as the Valuation Cap).

term sheets

SAL have provided two model term sheets for series A financing transactions. One is short form and the other a more detailed term sheet. As the short form version is 7 pages and the long form 24 pages, we expect the short form document to be used more often in the market.

Both term sheets include options for dealing with material provisions, for example the liquidation preference. On most series A deals in Southeast Asia a 1x non-participating liquidation preference is adopted, but this is not hardwired into the template term sheets. On the other hand, the templates assume that anti-dilution will always be calculated on a broad based weighted average basis – which reflects market practice.

Generally, the templates cover the key points that we would expect to see in a series A term sheet and we are happy to use the short form template as a starting point. In terms of any omissions, there is currently no reference in the term sheets (nor in the shareholders’ agreement) to any founder vesting arrangements. The intention may be to document this in a separate template, yet to be created.

subscription agreement

The subscription agreement is a balanced document, broadly reflecting market practice. It assumes that founders will be personally responsible for the reps and warranties alongside the company, but there are reasonable limitations on that liability, including separate financial caps for both founders and the company.

We don’t think that founders will find the warranty schedule any more onerous than usual. Indeed it doesn’t go as far as some subscription agreements we see – omitting for example specific warranties on data breaches, cyber security and anti-corruption policies / compliance (although these items are most likely captured in the more general compliance warranties anyway).

Finally, the subscription agreement assumes a single closing. It will need to be amended for a rolling close or tranched investment.

shareholders’ agreement

The shareholders’ agreement looks in good shape. The matters reserved for the approval of shareholders and/or the board look fairly reasonable. We expect that investors may add to them in practice. An ICO or other token generation event is included as a restricted matter. One item that founders should note are the forward-looking business undertakings, which are not always included in Southeast Asia funding documents. These include items such as taking steps to protect intellectual property rights, compliance with laws and obtaining insurances.

The term sheets are silent on the topic, but the shareholder’s agreement requires the parties to use their best endeavours to provide an exit within 5 years. If a trade sale or IPO is not achieved within that period, investors can require the company to appoint a third party to advise on exit strategy. At series A stage, we think it is too early to be imposing exit obligations (and that, if included, 5 years is too short a timeframe).

summing up

The SAL documents are a great addition to the Singapore startup ecosystem. We anticipate using them on deals where we are drafting the investment documents for the investee company. It remains to be seen whether investors will use the templates when they are leading on document drafting – particularly those VC funds with their own standard form documents.

We will follow up with some further guidance on the templates soon, to help founders with their review, noting of course that the development of these documents was driven mainly by investors.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

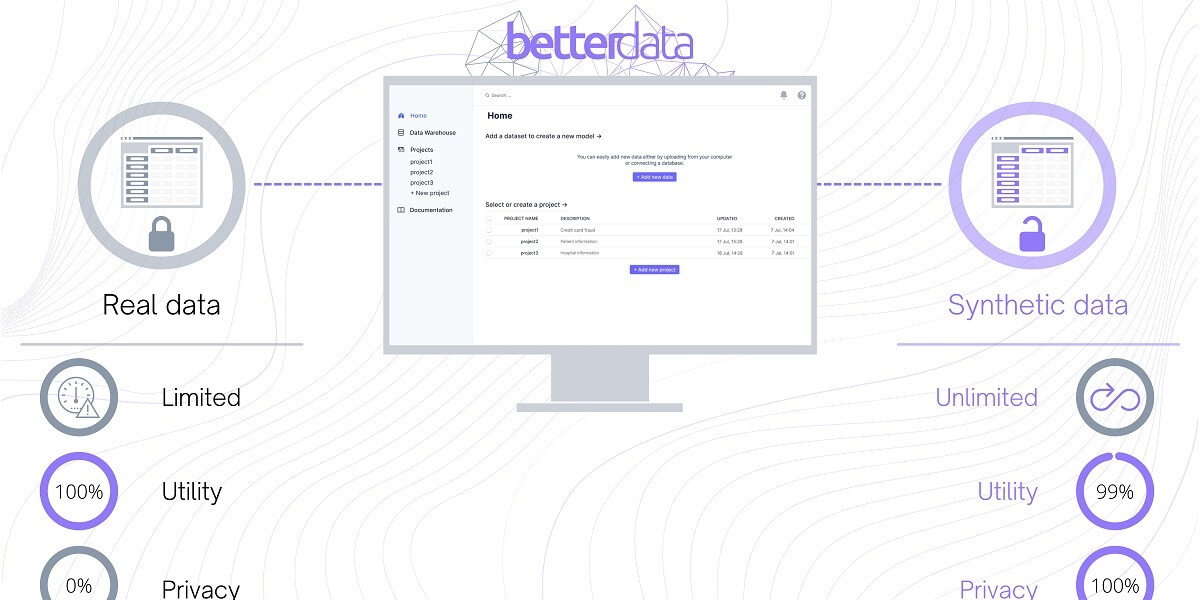

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.