our guides

explore our comprehensive legal guides on startups, capital raising, and more.

Employee share option plans (or ESOPs) are a key tool for startups to incentivise staff and hire talent when funds are tight.

However, not all ESOPs are made the same. To make it easy, we’ve put together this guide to help you through the main commercial questions you need to consider. If you want some guidance on the process of adopting your ESOP, setting up the option pool, and granting options, read our guide on how to set up an ESOP.

1) how big should your pool of options be?

Usually an ESOP pool is around 7.5-15% of a company’s total shares on a fully diluted basis (10% is most common). If you are setting up an ESOP as part of a capital raising transaction, your incoming investors may have specific requirements around this.

Generally speaking, founders are expected to take on the dilution from setting up an ESOP pool, and investors are not (i.e. an investor’s agreed stake in the company is calculated on a fully diluted basis, taking the ESOP pool into account even if the ESOP has not been formally put in place yet).

This means it’s important to make sure your ESOP pool is not significantly larger than required for your foreseeable hiring needs, as that chunk of equity comes out of your own pocket as a founder. Conversely, you’ll generally want to make sure you’ve set up a big enough pool to attract and retain the talent you’ll need.

2) how much will it cost employees to exercise their options?

The exercise price is the price that an employee must pay to exercise their options and is decided on a case-by-case basis for each employee. The exercise price is often set at the market price of the company’s shares at the time the options are granted (usually determined by reference to the latest completed funding round). Employees then benefit as the value of the company increases from the date they received their options.

3) how long will employees have to exercise their options?

The expiry date of an option is the latest date by which the option holder can exercise that option. This is typically aligned with the expected time frame for the company to find an exit. Typically in Southeast Asia this will be 7-10 years from the date of grant, but of course this depends on your company’s stage and maturity.

The expiry date may change if an employee ceases to work for the company. The most employee-friendly ESOPs do not change the expiry date if any employee leaves. Leavers are therefore not forced into exercising options prior to an exit event. However, some companies prefer to give leavers a shorter time frame, for example up to one year after leaving the company to exercise any vested options. This lowers the company’s administrative burden of keeping track of departed employees who hold options.

4) what is the timetable for the options to vest?

Options almost always vest over a 3 or 4-year period. Vesting incentivises employees to stay with the company throughout the vesting period, in order to be able to exercise all of their options in the future. Generally, if an option holder leaves before the end of the vesting period, he or she will lose their unvested shares.

Our template ESOP rules allow for recipients to have personalised vesting schedules on a case-by-case basis. Shorter vesting periods may be appropriate for employees who have already worked for the company for a significant period of time prior to receiving options.

5) what happens at an exit event?

This is likely to be the part of your ESOP which requires the most thought.

Our template rules provide for single-trigger acceleration on an exit; that is, all unvested options vest on an exit event and can be exercised in full. Single trigger acceleration is the most employee-friendly position and encourages all parties to push for an exit as soon as possible.

However, potential acquirers of your company can be put off by single trigger acceleration, as they often want key employees to stay with the business after the acquisition (and the continued vesting of options encourages that). Some companies therefore prefer double trigger acceleration in order to make their company as attractive an acquisition target as possible.

We find there is a lot of variation in Southeast Asia on this point. Single trigger remains the most common, as compared to the US, where double trigger acceleration is more usual.

The different scenarios are summarised below:

| no acceleration

| None of the unvested options vest on an exit event, and any unvested options expire. Option holders can only exercise options which have vested. |

| partial acceleration

| A set percentage of the unvested options vest on an exit event. The remaining options continue to vest in accordance with the vesting schedule. This can be important to a buyer where employees remain employed by the surviving entity, so that they continue to work for the business and earn their options. However, it can be less appealing to employees, who will lose unvested options even if they are terminated without cause. |

| double trigger acceleration

| A set percentage of the unvested options vest on an exit event. The remaining options vest on a second trigger, e.g. the employee being terminated (or resigns with good reason) in connection with, and within a certain time after, the exit event. That way, if the second trigger event does not occur, the employee must stay with the company in order to earn their remaining unvested shares. However, if a buyer does not choose to keep an employee after an exit, the employee is not penalised for this. In Southeast Asia, we do not see double trigger acceleration very often but expect that to change as some of the larger tech companies adopt Silicon Valley practices. |

Despite ESOPs being a common feature of many startups in Southeast Asia, their implementation can vary according to founder and investor needs. If you would like to discuss drafting an ESOP for your own startup, you can contact us.

introduction

Many seed investment rounds in Southeast Asia complete using convertible note instruments like the 500 Startups Keep-It-Simple-Security (KISS). These are unsecured debt instruments that convert to equity when a company completes its next equity raising.

In this guide we cover the 8 key features you should know when working with a KISS convertible note. From our experience, the KISS is the most common type of convertible note used in Southeast Asia. If you are contemplating a seed round, we suggest you upskill on this document by downloading a version of the KISS adapted for Southeast Asia from our website.

There are other forms of note in use in Southeast Asia, including US style documents. With these documents, US specific provisions need to be amended, e.g. removing US securities law and taxation language which shouldn’t be relevant for a non-US issuer.

an overview of how convertible notes work

Convertible notes anticipate that the investment amount is drawn down either in a lump sum on one date or, more likely, over a period of time. The investment amount typically automatically converts to equity on the date of a qualifying capital raise at a discounted price to the next round price, but subject to an overall valuation cap.

If not already converted, the debt may be repayable (potentially at a multiple of the outstanding amount) or convertible at the noteholder’s discretion:

key features of convertible notes in southeast asia

| Investment Amount | The amount to be invested by the investor (noteholders) |

| Series | Notes of a particular series are issued on the same terms. Typically, you may have a period of time to issue further notes on the same terms without seeking the consent of existing noteholders. The total investment amount is sometimes drawn down in a lump sum on one date or over a period of time with multiple closings |

| Interest | This is the annual rate at which interest accrues on the note whilst it is outstanding. In Southeast Asia, the rate varies, but usually is a low amount, e.g., 1% or 2% |

| Maturity Date | This is the date on which the debt is due for repayment. This should be a reasonable period of time from the date of the note, so that the company can achieve the qualifying capital raise (see below) to trigger conversion. In Southeast Asia, periods to maturity are generally set at 18 months and can be longer. Usually, if the company is unable to raise money before maturity, the majority of noteholders can elect for the debt to convert to shares rather than demanding repayment |

| Qualifying Amount | The investment amount of the notes will automatically convert into shares at the time of the company’s next capital raise. There is normally a minimum amount that must be raised to trigger conversion (called a qualifying capital raise), which is set to ensure that the raise is a legitimate company financing, not a device to trigger conversion |

| Discount | Assuming the company’s next financing round is a qualifying financing, the notes will automatically convert into shares often at a discount to the share price paid in that financing. The discount is intended to compensate investors for the risk they take on by investing at an early stage. In Southeast Asia, this discount is typically 15-25%. This follows Silicon Valley norms |

| Valuation Cap | This addresses an initial concern that investors had with the KISS style and other convertible notes – that the company’s valuation could increase significantly and they would only have the protection of the discount to the price of the next funding round. The valuation cap effectively caps the price at which investors pay for their shares when the note converts. If your company raises a financing round at a $5 million pre-financing valuation but the convertible notes have a $2 million valuation cap, your note holders will effectively receive a 60% discount to the price that the new investors are paying. So consider a valuation cap carefully as it can have a significant dilutive effect on the next round of financing if set too low |

| Majority-in-Interest | This term simply means those noteholders holding a majority of the total investment amount of the series. It is useful to incorporate this concept into the document so that key decisions are taken, or rights waived, not by individual investors but on a majority rules basis |

Interested in learning more about the mechanics of the convertible note, or have a term sheet that you want us to take a look at? Get in touch.

At some stage, startups in Southeast Asia may want to flip (or redomicile) into Singapore, which has legal impacts. Here’s the lowdown on why you might, when you should, and what’s involved.

why should a startup think about moving to Singapore?

It depends if your startup is choosing to bootstrap or seek venture capital. If as a founder you are considering VC money, you need to be mindful of investor preferences. When investors put money into startups, they prefer a safe haven to ensure they can enforce their rights under investment documents, and get their money out easily on exit. In Southeast Asia, that generally means investing into a company from a stable jurisdiction such as Singapore.

There are other drivers of course which can be relevant when choosing jurisdiction – protection of intellectual property rights, taxation, local-foreign ownership and capital requirements. Again, Singapore ticks most of the boxes.

when should a startup move to Singapore?

The easiest way to avoid the company secretarial and legal costs associated with flipping is to not flip at all – i.e. by incorporating your holding company from the outset in the most investment friendly place. That’s not always possible of course for various reasons.

If you do decide to redomicile your startup, then the earlier you act the better. Otherwise, the potential restructuring can be harder. For instance, intellectual property rights and key financing, commercial and employment agreements may need to be assigned to the new holding company.

Startups are often pressured to flip at the same time as a proposed capital raise, typically at the request of investors. Founders should exercise caution here. Terms sheets are non-binding and promises of investment based on the company flipping may not materialise into an actual investment.

how do you flip or redomicile a startup to Singapore?

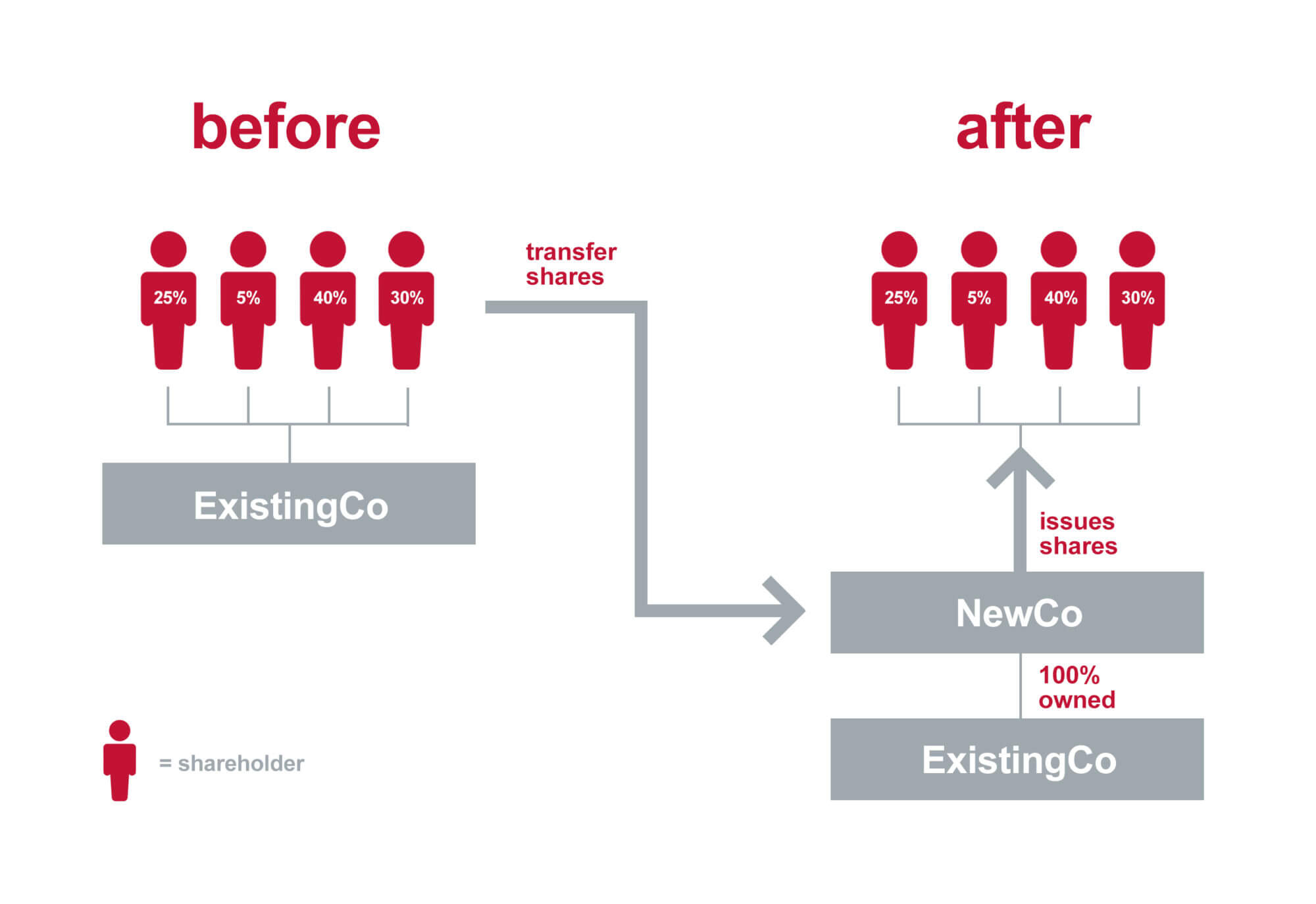

Flipping to a new jurisdiction can be done by either a transfer of shares (see diagram 1) or a transfer of assets (see diagram 2).

option 1: share transfer (most popular approach)

A share transfer is the simplest and most common approach. It works like this:

- you set up a new holding company in Singapore (NewCo)

- the Existing Company (ExistingCo) transfers all of the shares in ExistingCo to NewCo.

- NewCo then immediately issues shares in NewCo to mirror the holdings that had been held in ExistingCo.

Here are a few things you will need to consider if you flip via a share transfer:

- these are separate corporate transactions in two different jurisdictions. As a result, it’s a good idea to get legal and tax advice on both. For example, the share transfer may be a liquidity event in certain jurisdictions triggering a tax charge on the deemed capital gain.

- you need to attribute a value to the ExistingCo shares being transferred for the purposes of recording the share issue. This may mean you need to consider your company’s current valuation at the time of the transaction.

- although shares are being issued, no money is paid for the shares. You will need an agreement setting out the terms of this non-cash consideration. Our share exchange agreement is a useful template to record this kind of transaction. If you choose to use our share exchange agreement, you’ll need to have the agreement reviewed with local lawyers for compliance.

Overall, this is a fairly straightforward process on the Singapore side and can be done fairly efficiently with a lawyer and a corporate secretary working together, but can differ in cost and speed depending on the lawyers that you use in your home country.

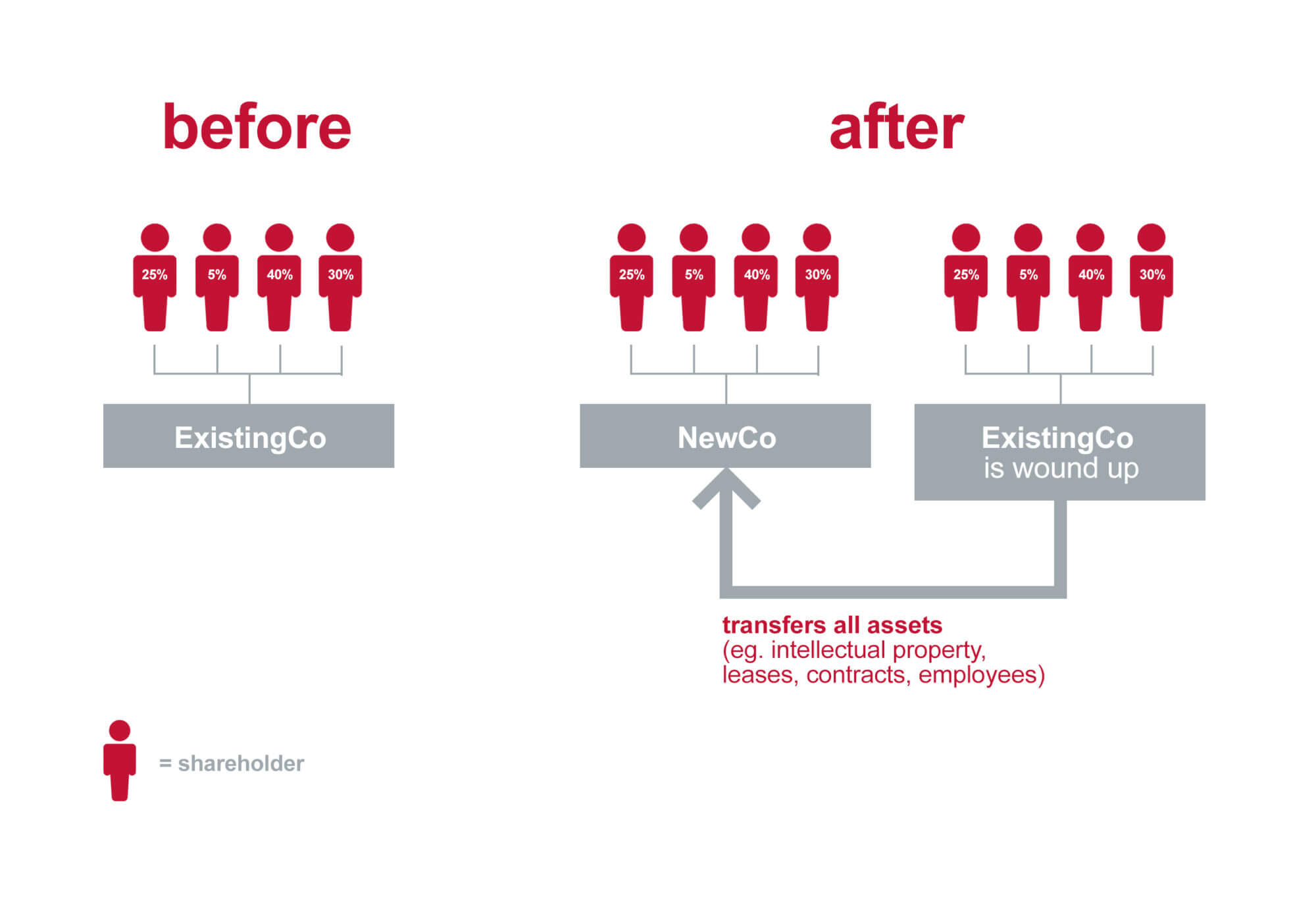

option 2: asset transfer

Flipping your company by way of an asset transfer is usually more complex because it requires the sale of individual assets from ExistingCo to NewCo. Given this, an asset transfer is only used if there are legal, tax or commercial issues with a share transfer.

An asset transfer involves assigning or transferring intellectual property, key assets, contracts and employees. These assignments and transfers may require the consent of third parties.

This process usually leaves ExistingCo without any assets other than either shares in NewCo or a debt from NewCo (the consideration or amount ‘paid’ for the asset transfer).

issues to watch out for when flipping your company into Singapore

- you will need to carry out some due diligence on your own company before flipping it. Aside from local legal and taxation matters, check whether existing contracts and other arrangements will be impacted by the redomicile, e.g. a shareholders’ agreement will need to be mirrored and restated under the laws of NewCo’s jurisdiction.

- the transfer of shares needs to be executed in the same way as any other share transfer, i.e with the usual stamping, approvals and registrations that are required under the applicable law. However, as no cash passes, you need to check how the transfer needs to be recorded for accounting and tax purposes.

- check any existing contracts you have. The share transfer may constitute a change of control or liquidity event under existing commercial contracts, financing documents or leases. You should review existing documents and get consent from third parties, if required.

- convertible notes issued to investors will need to be reissued by, or assigned to, the NewCo, as will any founder vesting agreements in place.

- any share option plan will need to be cancelled, restated at NewCo level, and adapted for local law and standards.

If you’d like to get more information about what’s involved with a company redomicile, speak to us.

In the last few years, convertible notes have been frequently used on Singapore financings. Perhaps less common has been the use of SAFEs – the instrument created by Y-Combinator (YC) several years ago. However SAFEs are on the increase on fundraising deals across Southeast Asia.

Two years ago, YC reinvented the SAFE and launched what is now known as the ‘post-money’ SAFE. And just last month they released beta versions of the “Valuation Cap, no Discount” post-money safe and side letter specifically for companies registered in Singapore. You can access these here.

quick reminder – what’s a SAFE?

A simple agreement for future equity – in short, it’s an instrument convertible into shares similar to a KISS or convertible note. What’s different with a SAFE is that it doesn’t typically have any interest accruing, nor any maturity date and repayment obligation. They are therefore seen as a founder friendly investment tool to raise capital.

Like KISSes and other convertible notes, SAFEs typically convert into shares on the basis of a conversion price which is usually an agreed discount to the price of the next equity round, but which is subject to an overall valuation cap – i.e. whichever gives the lower price for investors.

so, what changed with the ‘post-money’ SAFE?

post-money SAFEs don’t dilute each other (bad news for founders)

The main change is that the new SAFE uses a post-money valuation cap instead of pre-money. The drafting change is fairly subtle to see: the definition of Fully Diluted Capital in the SAFE is amended to reflect the new principle. However, the impact can be significant. It means that the company’s valuation for calculating the conversion is “post” (i.e. after) the conversion of any other SAFEs or convertible instruments issued by the company, but prior to the valuation of the company immediately after the equity financing round. This results in further dilution for founders on conversion and potentially to any other investors that do not hold post-money SAFEs.

Just to be clear and to dispel a myth, by ‘post-money’, this is post all other SAFEs and convertible notes, but not post the next equity financing as well, as some founders have asked. That really would cause dilution!

Under post-money SAFEs, the post-equity financing option pool is no longer factored into the pre-money calculations, which actually benefits founders from a dilution perspective. Under the original SAFE, option pool expansions resulted in SAFE investors receiving additional shares. However, overall this doesn’t balance out the additional dilutive effect outlined above.

you’ll only feel the impact with multiple rounds of SAFEs

It is worth pointing out that for a company that only ever raises one SAFE investment round, a post-money SAFE has no real impact. Rather, it comes into play when more than one series of SAFEs or other convertible notes are issued. In Singapore, we perhaps see this less commonly than say in the US where substantial amounts are often invested using SAFEs and other convertible instruments, and not only in the first round of investment.

easier to calculate cap table (good news for founders)

YC’s view at the time of launching the new SAFE was that it makes the maths simpler for everyone and creates more certainty over ownership and dilution. Which is probably true. But if you issue more than one round of SAFEs or other convertible notes, and you use post-money SAFEs, founders will likely experience more dilution on conversion than they would have done under the original YC SAFE, simple as that.

In light of this, if presented with a post-money SAFE, founders may want to negotiate up the valuation cap to mitigate against the dilutive impacts potentially coming into effect.

what else did YC change?

The original YC SAFE granted holders a pro-rata right on the next financing round. The new SAFE doesn’t automatically include this. Instead, YC put out a separate side letter on their website under which these additional pro-rata rights might be granted.

Also, the old SAFE could only ever be amended by the holder. The new SAFE on the other hand permits amendments by written consent from a majority of SAFE holders. This is something we think is valuable on all convertible instruments, i.e. the holders effectively make decisions on a consensus basis, avoiding one single small investor taking a different view holding things up.

other key points to remember about a SAFE

Not specific to the new post money version, but whenever drafting or reviewing a SAFE, keep these tips in mind:

- Look out for most favoured nation (MFN) provisions. These enable early investors to have the benefit of any rights granted to future SAFE holders which might be more beneficial. If nothing else, it can be a burden reissuing new SAFEs on these better terms to lots of prior investors.

- SAFEs typically convert automatically on completion of the next equity financing. There should ideally be no minimum amount to be raised to trigger this automatic conversion under a SAFE. Some investors like to include a threshold to ensure it is a legitimate fundraising round. Always be careful you do not go too high with this so as to prevent automatic conversion of the SAFE.

- A SAFE (like all convertible instruments) should include language to the effect that, on conversion, holders will only have the benefit of their lower conversion price for the purposes of liquidation preference and anti-dilution rights. This can be achieved through issuing a separate class of “shadow” preferred shares, or just by drafting carefully the relevant provisions in the constitution and shareholders agreement put in place on the equity round.

round up

If you are presented with any kind of SAFE right now, it will most likely be the post-money version, so come and have a chat to us.

Traditionally, growth stage technology companies in Southeast Asia have raised venture capital via convertible debt or equity rounds. However, venture debt is fast becoming an alternative or complementary path for startups looking to get capital to accelerate their growth. In this guide we cover the basics of venture debt. For more detail, download our latest free e-book, The Startup Guide to Venture Debt in Southeast Asia.

what is venture debt?

Venture debt is a form of debt financing, similar to bank loans but with a few key commercial differences. Venture debt is typically used by VC-backed, fast-growing tech startups that may not have positive cash flow or significant assets to use as collateral. These companies are typically not eligible to receive traditional debt financing from banks or other institutional lenders (or would only be able to borrow at prohibitive interest rates).

is my company a good candidate for venture debt?

The typical profile of a company taking on venture debt is a venture backed, fast-growing startup at series A or later. By the time a company is ready to explore venture debt, it will already have cashflow and an established customer base. Venture debt lenders also prefer venture-backed companies (i.e. those who have received funding from VCs / institutional investors). Institutional investors will have ‘vetted’ the company, and can be a future funding source should the company need help in paying back the venture debt.

why go for venture debt instead of an equity round or convertible debt?

There are a few reasons why a company may use venture debt as an alternative, or supplement, to equity financing:

- less dilution: founders retain more of their shareholding

- board control: venture debt lenders typically do not require a director seat

- transaction time: the process is generally faster than an equity round, since lenders ‘piggy-back’ off the due diligence of the institutional investors.

learn more about venture debt and the process

If you’re looking for more information about types of venture debt, key terms to negotiate in your venture debt term sheet, and details of venture debt providers in Singapore, download our free PDF guide.

You can access the guide by filling out your details below:

Atlassian made a splash in the tech M&A world recently by publishing their term sheet for strategic acquisitions.

So why has Atlassian gone public when acquisition terms are generally a closely guarded secret? Atlassian’s stated aim is to make the M&A process fairer, more efficient, and less painful for sellers.

We assume another driver is to position Atlassian as a seller-friendly buyer in the hyper-competitive tech M&A marketplace.

Has Atlassian achieved its goal(s)?

The Aussie tech legend scores brownie points for transparency. The traditional approach of keeping acquisition terms hidden allows buyers to claim their term sheets are market standard. This chestnut makes it hard for first-time founders to negotiate, as there is no easy way to judge whether particular terms are standard or harsh (or where on that continuum a term falls).

As Atlassian notes in its blog, making this information available to prospective sellers should make the negotiation process easier.

Atlassian also deserves credit for putting forward some seller-friendly terms.

Here’s our rundown of things we like in the term sheet and a couple of things that make us go hmmmmm.

three things we like for founders looking to sell

favourable escrow terms

It’s common for us to see buyers holding back at least 10-20% of the purchase price in M&A deals against warranty claims for up to 2 years post-closing (this is called escrow). Atlassian’s terms mean more money in sellers’ pockets upfront when the deal closes. The maximum ask is a 5% escrow if the deal is under $50m.If it’s over $50m the seller can choose between either i) a 5% escrow, or ii) a 1% escrow and footing the bill for Atlassian’s reps and warranties insurance covering up to 4% of the purchase price). In each case Atlassian is comfortable with a 15-month escrow period.

Atlassian’s escrow terms are substantially more attractive than those commonly offered to sellers in tech transactions.

a practical approach to general warranties

Atlassian caps the sellers’ liability at the escrow amount for general warranty claims (including IP warranties). There is also a 15-month claim period. We’ve seen warranty liability capped at anywhere from 25%-100% of the total purchase price, and claim periods of 12-24 months. Atlassian’s terms are therefore pretty friendly to sellers.

ESOPs covered upfront

The term sheet explains how Atlassian treats existing ESOPs. Generally speaking, vested equity is cashed out, and unvested equity is terminated and substituted for an Atlassian scheme. We’re happy to see Atlassian raising this upfront – share scheme details can sometimes be inadvertently left out at the term sheet stage, causing problems down the track.

things that make us go hmmmm (for founders looking to sell)

exposure outside the scope of general warranties

Liability for anything outside the scope of the general warranties is pretty tough – capped at 100% of the purchase price and subject to a claims period of the statutory limitation period, or 6 years (whichever is longer). This special basket includes tax warranties and indemnities dealing with specific issues picked up in due diligence. In the Southeast Asian context, 6+ years isn’t unusual for tax claims but is a long claims period for most other issues, which we think will be unattractive to many founders and sellers.

restrictions for core employees

Core Employees (typically founders) identified in the term sheet will receive a percentage of their purchase price in Atlassian shares that vest quarterly with a 1-year cliff. The core employees are also required to enter into non-compete and non-solicit undertakings. Hard-baking some of the purchase price in stock that is subject to future vesting is a bit tough on those founders who have long been fully vested.

However, this may not be a big concern if only a small percentage of the purchase price to be paid in stock – Atlassian has left this silent in the term sheet for now.

waive goodbye (maybe) to benefits

Atlassian reserves the right to require team members to waive existing vesting acceleration rights, change-in-control payments, severance compensation, or other payments that might be triggered by the acquisition. This is sometimes seen on Southeast Asian transactions, but is usually open to negotiation.

tipping basket

Atlassian expects to be able to bring warranty claims once the total minimum value of all warranty claims hits 0.5% of the purchase price (known as the tipping basket in the U.S. and as the de minimis amount in Southeast Asia). 0.5% does seem a bit low to us but we don’t tend to see sellers die in a ditch over this point..

reverse triangular what?

The term sheet assumes the transaction will be structured as a reverse triangular merger – a structure popular in the US for tax and other reasons. Reverse triangular mergers are not something to be attempted without adult supervision. Expect to spend some money on tax and legal advisers if you need to get your head around this.

It’s great to see such an open discussion by Atlassian of their term sheet and process, and we look forward to seeing whether other regular tech acquirers follow suit.

This article was co-authored with Fiona MacKinnon from our Wellington office.

The global economic downturn has inevitably hit the startup and venture capital ecosystem. Investors in startups, like everyone else, are impacted by falling stock prices and fund valuations, distracted from investing new money and busy supporting existing portfolio companies. These factors make it harder for startups to raise money right now.

But for those startups that are still raising money, what is the approach of investors? Is the VC term sheet about undergo a change?

valuations

Startup valuations are falling. For those companies that have raised a previous round of financing, founders will want to avoid a down round – a fundraising in which a company issues shares at a lower price than the previous investment round – at all costs, as doing so may trigger investors’ anti-dilution rights. If anti-dilution rights are triggered, founders could face significant further dilution.

If company cash is low, existing investors may need to support a new financing. If so, founders will need to negotiate hard with both new and existing investors. Anti-dilution rights can be fully or partially waived on a fundraising at the end of the day. If anti-dilution rights are triggered, founders may then need to ensure that they remain sufficiently incentivised following the dilution, for example via an increased portion of the company’s ESOP.

extension rounds and convertible notes

Extension rounds at the same price as the last financing round may be an alternative to a down round. With no increase in valuation, startups will want to classify such investments as a bridge or extension. Therefore, expect to see investment rounds using preference share class terminology such as series A2, series B+, pre-series A or similar.

We also anticipate more convertible notes will be used in the market. This not only avoids initial dilution but pushes the whole difficult discussion on current valuation to another day. This, of course, also has its disadvantages. To some extent, founders are just kicking the valuation debate down the road and it will still have to be addressed at some point. In the current market, it also seems inevitable that SAFEs will be less common than traditional convertible notes carrying repayment obligations. We also expect investors to be more aggressive on setting lower valuation caps and fluctuating price discounts depending on the timing of conversion into equity.

tranched investments

Now is the time to get money into the business to give it runway for a decent period of time. Tranched investments conditional on financial performance are best avoided by startups at the best of times. Right now, it is very difficult to forecast traction and performance over the next 12-18 months. Unfortunately, given the uncertain economic environment, investors may well think the opposite and insist on structuring investments in tranches subject to KPIs.

warrants

Warrants, which provide an option to purchase more shares at a future date at a fixed price, may also be a tool for investors to use in the current environment. The exercise price of such warrants is key – the lower the price, the more potential dilution. If warrants are issued and/or exercisable down the line, based on company performance, the true share price of the financing round may be considerably less than initially agreed.

redemption / buy-back rights

Investors sometimes include redemption or buy-back rights which entitle them to their money back in certain circumstances. Usually this is where there is some kind of event of default by the company or its founders.

However in difficult times, investors tend to broaden the circumstances in which such redemption or buy-back rights can be enforced (e.g. financial performance deteriorates or being unable to satisfy a key commercial arrangement or deliverable). In this uncertain economic period, investors may look to de-risk transactions even further using such a mechanism. Founders should be cautious about agreeing to any broad redemption or buy-back rights triggered by anything other than a material breach or default.

liquidation preference

Liquidation preferences provide investors with downside protection if a company is either sold or wound up. In such an event, investors are entitled to receive an agreed amount of the proceeds before anything is paid to other shareholders. During the good times, founders and startups have become accustomed to 1x non-participating liquidation preference in most cases – a generally accepted VC market standard. With stormy clouds above, we can expect that to change, with liquidation preference carrying higher multiples, and also participating preferences returning.

Further, for companies that have raised previous rounds of investment, incoming investors are more likely to seek a senior class of shares, than rank alongside existing preference shareholders, which is common in normal market conditions.

exit rights

Exit rights give investors a way to sell their shares if the company hasn’t got to a liquidity event (e.g. a trade sale or IPO) within a set period. We may see shorter time periods before these rights kick in. The remedies provided to investors vary, but we could see more instances of the following:

- a right to require the company to buy-back investors’ shares at a specified price (for example, based on fair market value)

- investors having the option to reconstitute the board giving them greater voting control

- an obligation on the board to engage an investment banker to find a buyer, coupled with a drag-along right so that shareholders (including founders) can be forced to sell at a price determined by investors

venture debt

Finally, venture debt is likely to become a more important source of financing in the short term, in most cases complementing an equity financing. As an alternative capital raising option for high growth companies, venture debt is a good option for entrepreneurs looking to extend their runway, using an instrument that results in less dilution.

round up

Right now VC firms and other investors will be taking a closer look at downside protection in their term sheets. Of course, not all investors are predatory, nor will the majority take advantage of the difficult economic climate to seek further influence in startups. But now is certainly the time for founders to reach out to lawyers at the term sheet stage to understand what is, and what isn’t, market standard, and how this may be changing.

This guide is for founders who have recently started their own business and are preparing for their first round of funding. The guide sets out six things you should consider:

- founder vesting

- remuneration arrangements

- intellectual property

- cap table

- corporate secretary

- due diligence folder

Our suggestions in this guide assume that you want to raise money from a professional investor such as a VC firm, angel group, or incubator, i.e. investors that are likely to carry out some form of due diligence and will want formal legal documents put in place as part of the funding round.

In contrast, friends and family type investors are often willing to invest without going through a formal due diligence process, meaning you may not need to do as much legal housekeeping to secure their investment.

1 founder vesting

Where you have two or more founders in your startup, it is worth having a conversation about how much time and for how long each founder will contribute to the business. Typically, founders intend to work full time for the foreseeable future. However, it is possible that personal circumstances like a family illness or career opportunity might make a founder wish to move on earlier than anticipated.

Because of this, it is common for founders to sign a founder vesting agreement. These agreements state that a founder only unconditionally owns of all his or her shares after having contributed to the business for a certain agreed period. If a founder leaves during the vesting period, a proportion of the shares can be bought back and cancelled by the company for nil (you can read more in our comprehensive guide to founder vesting).

It is better to set these expectations on all founders earlier rather than later, when relationships are good and before you get into the fundraising process.

Founder vesting agreements are different to shareholders’ agreements, another common legal document. Shareholders’ agreements are more comprehensive, and set out most of the rules which govern how a company is to operate.

We generally suggest holding off putting your first shareholders’ agreement in place until you meet an investor who requires you to have one. Almost all of the provisions of a typical shareholders’ agreement are relevant only after you bring in a material outside investor. Putting such an agreement in place too early tends to be a bit of a waste as you will almost always have to terminate and replace it at the time of your first investment.

(Click here to download our founder vesting agreement template)

2 remuneration arrangements

employees and contractors

Broadly speaking, you can remunerate those who provide services to your startup through cash or equity (or a combination). Every person that you hire as an employee or contractor should have an employee agreement (the Ministry of Manpower’s template is available here) or independent contractor agreement.

(Click to download our independent contractor template.)

advisors

For early stage startups, it is common to engage a third-party advisor (or advisors) who the founders can glean industry insight or other expertise from when trying to work out how to take their idea to market, scale-up, and so forth. The advisors will sometimes be granted shares or options in return for their advisory services (typically set out in an advisor agreement) if they are providing material value to the company.

Whether you should pay such an advisor using shares or options is often driven by the cash resources at the time, but founders and advisors should note that the advisor may have tax consequences of receiving equity for services.

(Click to download our basic advisor share agreement template.)

employee share option plans (ESOPs)

We are often asked whether an early stage company needs to put an employee share option plan in place. Most investors ask startups to establish an ESOP as part of the first funding round. They will not expect the company to already have an ESOP in place and so we normally advise founders to hold off on their ESOP until this time (unless they have an urgent need to grant options to employees for retention or hiring purposes).

3 intellectual property (IP)

Tech investors will usually want to be certain that the company owns all of the IP necessary to run its business, or at least, holds valid licenses to use that IP.

different types of IP in a business

Intellectual property can be loosely divided into two types: IP that can be registered (e.g. patents, trade marks and registered designs), and IP that cannot (e.g. most software). Most startups only have unregistered IP.

Patents are difficult to obtain but may be worth applying for in some circumstances.

Although investors are usually less concerned about this, it is always worth considering registering your business trade mark, as a means of safeguarding and commercialising your company’s brand.

how to document your IP

Whatever the form of your IP, it is important to document the ownership of that IP by your company.

The most common way of doing this is by having each founder, employee and contractor sign an employment or contractor agreement. Those agreements should include a clause that states that the company owns all IP created by the founder, employee, or advisor during the term of the agreement.

If IP was created before a founder, employee, or contractor entered into a services contract, this pre-existing IP can be transferred to the company using a deed of assignment of IP.

(Click to download our independent contractor template.)

(Click to download our deed of IP assignment template.)

4 cap table

Most investors will ask you to send them a cap table that sets out your existing shareholders and the number (and class) of shares held. The cap table might need to set out any other rights to subscribe for shares in the company (e.g. convertible notes, SAFEs, or outstanding options).

If you have a share option plan your cap table will not usually be exactly the same as the electronic register of members (EROM) on ACRA. This is because a cap table typically shows the fully diluted position (which assuming all options have been allocated) whereas the EROM only shows the shares in issue.

(Click to download our template cap table.)

5 corporate / company secretary

All companies are required to have a company secretary from incorporation. We suggest making sure that your company secretary is one that knows how to handle the sort of directors’ and shareholders’ resolutions and approvals you will need to establish an ESOP, issue shares on the conversion of investments made under convertible notes, issue shares with preferential rights and so on.

6 due diligence folder

We suggest keeping a Google drive, Dropbox or similar folder that keeps copies of your key company documents in one place. For starters, it should include:

- your ACRA Bizfile

- your constitution

- the other documents mentioned in this article that you have in place (i.e. any founders agreements, employment agreements, advisor agreements, etc)

Having this folder will allow you to quickly and easily provide potential investors with access to these key documents. This will make the company look well organised to potential investors when they are making an initial investment decision and will speed up the process when they are undertaking due diligence.

conclusion

Most startups do not need to have complicated paperwork in place prior to seeking investment. Your key focus should be on developing the business and creating a compelling product and/or service.

Nevertheless, it is good practice to have some or all of these arrangement in place in advance. Fundraising is a high friction activity at the best of times, but having your ducks in a row at the start of the process should make it as smooth as possible and save you a few headaches along the way!

Kindrik Partners has a library of 30+ templates and guides for startups, including guides on capital raising. Read our guide on seed rounds or if you have any questions, get in touch with one of our venture capital lawyers.

This short guide demonstrates how founders should calculate the number of options to include in their ESOP pool.

For the purposes of this example we have assumed that the founders are setting up a customary 10% ESOP pool (check out our guide 5 key questions when setting up an ESOP for a more detailed discussion on the appropriate size of your ESOP).

example

In almost all cases you should calculate the size of your ESOP pool on a fully diluted basis. i.e. the ESOP should be equal to 10% of all shares and options on issue (including the ESOP). Looking at a company with 1,000,000 shares on issue:

tool

If you are experiencing some arithmetic fatigue, we have you covered. Available for free download here is a spreadsheet tool that incorporates the above formula. All you need to do is plug in your total number of shares and options on issue, your ESOP pool size as a percentage, and the tool will generate the relevant number of ESOP pool shares.

Advisors help startups by offering expertise or perspectives that the core founder team may not have. Since most startups don’t have the cash to compensate these advisors, a common way to pay for their guidance is to offer equity.

We are often asked how companies should best go about this. In this guide we cover the types of advisor equity (shares versus options), how vesting can be incorporated, what else to cover, and other common questions.

types of advisor equity

When offering equity to advisors, there are two common roads to take: either giving shares, or granting options. The fundamental difference between shares and options is that if someone owns shares, they are immediately a shareholder in the company. If someone owns options, they have the right to purchase shares in the future.

share issue

Shares are a straightforward way to compensate an advisor. In most cases, advisors prefer shares rather than receiving options under the company’s option scheme. Like any share issue, the company will need to pass board and shareholder resolutions, as well as receiving necessary waivers and consents under the constitution and shareholders’ agreement in place. For that reason, a company intending to issue shares to advisors in the future usually carves this out under the constitution and shareholders’ agreement in the same way as they would an ESOP.

granting options

Options are an alternative way to compensate an advisor, and can be granted easily if a pool of options (such as an ESOP) has already been established. However, often advisors can come on board before the ESOP is formally set up.

If options are issued to an advisor, in the event that the advisor wants to exercise their options and convert them into shares, they will need to pay the ‘exercise price’, which may be around the price that the investors paid in the last funding round. This means that they will need to come up with cash to exercise their options.

how much to give?

There are different models to decide how much equity to offer. The Founders Institute gives a useful framework based on the stage of the company (idea, startup, or growth) and based on the various levels of engagement. This is really just a guide however.

| Idea Stage | Startup Stage | Growth Stage | |

| Standard: Monthly Meetings | 0.25% | 0.20% | 0.15% |

| Strategic: Add Recruiting | 0.50% | 0.40% | 0.30% |

| Expert: Add Contacts & Projects | 1.00% | 0.80% | 0.60% |

https://fi.co/insight/the-founder-institute-s-standard-advisor-agreement-for-startups-fast

vesting schedule

Advisor agreements typically have a vesting schedule of around 12-24 months, i.e. they are shorter than vesting schedules for founders and employees under an ESOP. This is because advisors generally bring greater value over a short term. As your startups grow, it cycles through different advisors that fit their applicable stage of growth.

Some advisor agreements also contain some measure of ‘claw back’ if the advisor does not perform make the expected contributions over the agreed period. An alternative to a provision like this would be using a cliff of 3-6 months to provide for a ‘test run’ to see if the relationship is beneficial.

other provisions

The advisor should agree that all intellectual property and other business, technical and financial information that the advisor obtains from the company or learns in connection with his or her services is appropriately assigned to the company.

As a minimum, the advisor should be subject to confidentiality provisions. You may want to add a no-conflict provision, and also a provision that the advisor complies with certain company policies.

Finally, there is usually a termination right for both parties and sometimes automatic termination if the company has not requested that the advisor render any services for a lengthy period.

tax implications

Options and shares are treated differently with regards to how they are treated in a tax sense. Generally speaking if you are issued shares for services, you would expect to have an income tax liability whereas options do not trigger a liability until exercised. We recommend obtaining tax and accounting advice before putting in place any advisor agreement.

advisor agreement template

We have produced a simple template agreement that a startup can use when bringing an investor on board. The template is drafted on the basis that the advisor receives shares, and that no cash compensation will be paid. It also provides that some of the shares may be clawed back by the company if the advisor fails to make the expected contributions over the agreed period, which is usually one or two years.

You can download our advisor share agreement template here. If you have any questions regarding the template or want to work with us to draft your advisor agreement, get in touch.

Lee Bagshaw presents this deep dive video series on negotiating Series A term sheets in Southeast Asia. The aim of the videos is to help startup founders understand the technical content of a typical term sheet, and to highlight the areas that are best to focus on in negotiations with potential investors.

The videos are based around a typical term sheet which you can download below. The term sheet is marked up from a startup founders’ perspective, and we recommend you watch the video with the mark-up in front of you as Lee refers to it often.

The first video gives a general introduction to the term sheet and explains how to approach negotiations with your investor. The rest of the videos dive into important terms contained in typical term sheets.

1. approaching the term sheet

2. investment terms, cap table and valuation

3. rights attaching to preference shares (part 1)

4. rights attaching to preference shares (part 2)

5. transfer and issue of shares

6. major share transfers

7. founder share restrictions

8. governance

9. default provisions, exit rights and redemption

10. transaction documents and closing

11. summary

(revised 11 February 2020)

introduction

Employee share option plans (or ESOPs) are a key tool for startups to incentivise staff and hire talent.

To make it easy, we’ve put together this guide to help you through the process of adopting your ESOP, setting up your option pool, and granting options.

Related guides you might also find useful:

- 5 key commercial decisions you need to make about your ESOP before you start (a good precursor to this guide)

- Tricky clauses: what happens to an employee’s share options when a company exits?

- Tricky clauses: what is founder vesting?

Ok, let’s get started. Here are the steps that you need to take in order to set up an ESOP in your startup. This is based on industry standard for startups that have a headco and employees based in Singapore – your mileage may vary for companies domiciled in other countries.

1. draft the ESOP rules

Your ESOP rules set out the terms that apply to all options granted under the plan, including the process for granting options, how and when employees can exercise their options, and what happens to the options on an exit event, or if an employee leaves.

If you’re using our ESOP, that document will include the following schedules:

- schedule 1 – a grant letter setting out the terms of the options you want to grant to recipients

- schedule 2 – the form of the exercise notice to be delivered to the company when an option holder wants to exercise their vested options

- schedule 3 – an option certificate which records the number of options, exercise price and vesting provisions.

2. approve the rules and the option pool

Once you are happy with your ESOP rules, your directors and shareholders will need to sign some corporate approval documents to adopt the ESOP rules and set up your option pool.

For Singapore companies, these resolutions will typically be prepared by your corporate secretary. If your company is based elsewhere in Southeast Asia, we recommend confirming this step with a local law firm.

board and shareholder approval

You should ask your corporate secretary to prepare a set of directors’ resolutions in writing for the directors of your company to sign and a similar set of shareholders’ resolutions in writing for your existing shareholders to sign. The resolutions should include the following:

- approval of the ESOP rules

- the total number of options in the ESOP pool.

- authorisation for the board to grant options to recipients of their choosing (up to the number available in the ESOP pool), and

- authorization to issue shares on any exercise of the options

shareholder waivers and consents

Your constitution and shareholders’ agreement (if you have one) may include pre-emptive rights on the issue of new shares.

If this is the case, those shareholders with pre-emptive rights will need to sign a waiver in respect of any options granted under the ESOP (and any shares issued on the exercise of those options). If required, you should ask your corporate secretary to prepare this shareholders’ waiver as well.

Finally, you should also check your existing constitution and shareholders’ agreement (if any) for specific consents required from any shareholder in order to issue shares, grant options, or establish an ESOP. For instance, if you have been through an external funding round, your investor may have a veto right over the issue of any new shares or options. If that is the case, you will need that party’s written consent to grant options and issue shares under the ESOP.

Now you are ready to begin granting options.

3. grant your options

Here’s what you need to do to grant options to selected recipients.

prepare your directors’ resolutions

Each time you want to grant options, you should ask your corporate secretary to prepare a new set of directors’ resolutions in writing, approving the grant of options to a specific recipient (or list of recipients).

send each recipient their grant letter

Send each recipient:

- a completed & signed grant letter (that includes the number of options granted, the exercise price, and the vesting schedule). Our template ESOP rules include a template letter of grant at (see schedule 1) which should form the base of each grant letter.

- a copy of the ESOP rules attached (note: the schedules attached to the ESOP rules themselves should be left blank in all cases.)

If the recipient accepts the offer, they should counter-sign the letter of grant and return it to you.

issue the option certificate

Once you have received the countersigned letter, you can issue them their option certificate.

In our ESOP rules template, you can find the option certificate form in schedule 3 (again that schedule should be left blank and a separate option certificate provided to the recipient – i.e. you need to create a fresh, separate Word doc).

update your option register

Internally, you should also be keeping an option register, which is a record of all the options the company has granted, the vesting schedules, expiry dates, and exercise dates.

how can an option holder exercise their options?

If an option holder wants to exercise their options, the first thing to do is check whether those options have vested in accordance with the option holder’s vesting schedule and have not expired under the ESOP rules.

If the options have vested, the option holder should deliver an exercise notice to the company. Our template rules include a template exercise notice that can be used for this. If you’re using our template rules, the process for exercising options is set out in Rule 5.3.

summing up

Setting up an ESOP is not too difficult once you have a set of ESOP rules that you are happy with. In most cases, your company secretary will be able to prepare all the necessary resolutions pretty efficiently.

The map of the funding terms is a tool to track typical investment terms that our VC lawyers see on fundraising deals at different stages of a company’s life cycle in Southeast Asia. It helps startup founders compare what is typical in the market when reviewing their own term sheets. To use the tool, click on the relevant term and you can review the position at each stage of fundraising.

If you are considering raising money for your startup in Southeast Asia, there are two main ways you can do it: either by giving away equity in exchange for money, or by using convertible notes. In this guide we explain how each approach works and the pros & cons of the different methods.

Other resources in our series on convertible notes:

- 8 key features of convertible notes in southeast asia

- KISS term sheet template (PDF & Word versions)

- KISS convertible note template (PDF & Word versions)

- SAFE convertible note template (PDF & Word versions)

what is a convertible note?

In simple terms, a convertible note is a loan that converts to equity when you do your next fundraising round – a qualifying capital raise. In other words, investors will loan money to a startup, and then rather than get their money back with interest, the investors will receive shares in the next round. Originally used more for bridging rounds, where money was given to make it to the next funding round, convertible notes are now very common in seed rounds.

There are two key features of a convertible note. One is that a convertible note will usually convert at a discounted price to the next round price. In other words, founders are trying to incentivise investors by saying, “if you invest in us today [when we’re a riskier bet], we’ll give you 20% off when it comes time to our Series A round”.

The second key feature is its valuation cap, which protects investors by putting a ceiling on the conversion price of the note and lets the investors share in any significant increase in valuation (that might have come as a result of their investment of money and resources).

types of convertible note

There are two main forms of note used in Southeast Asia: the KISS-style note used by 500 Startups, and the SAFE note based on the note developed by Y Combinator.

Under the KISS convertible note, the note is repayable on the maturity date (typically 18-24 months from the date of the convertible note) if it has not already converted to shares. The investor can also choose to be repaid the investment amount (or a multiple of the investment amount) on a liquidity event.

A SAFE note, on the other hand, is not repayable at the end of a fixed period, and the company must only repay the note if an insolvency event occurs, or if the investor chooses to be repaid on a liquidity event rather than convert their note. A SAFE is essentially a quasi-equity instrument, whereas as KISS is quasi-debt, because there is a contingent repayment obligation.

The KISS and the SAFE notes also differ in the ways that they can convert.

A KISS note converts:

- automatically when the company raises its next round (the qualifying capital raise);

- at the investor’s election when a liquidity event occurs (like the sale of the company); or

- at the investor’s election at the maturity date.

On the other hand, a SAFE note converts automatically when the company raises a qualifying capital raise, or if the investor so chooses on a liquidity event. The investor cannot force conversion after a fixed period.

There are also different types of SAFE notes, namely the pre-money SAFE and the newer post-money SAFE recently developed by Y Combinator. The difference between these is a substantial topic in and of itself – we recommend checking out some of the blog articles that others have written about it, like this one.

what is an equity investment?

Unlike a convertible note, under an equity investment, the investor receives shares in the company at the time of their investment. Where the investor is an institutional VC, those shares will typically be preference shares, which may carry the types of preferential rights we discuss in this guide.

pros and cons: benefits of convertible notes

From a founder’s perspective, the biggest benefit of convertible notes over an equity financing is speed. The note is generally a single document with simpler terms to negotiate, and without lots of conditions, representations and warranties.

In addition, the KISS and other most convertible notes are designed to be executed by individual investors, so it is possible to receive funds without closing with all investors simultaneously – a ‘rolling close’.

Here are some other benefits to using convertible notes:

- they postpone the difficult discussion about the company’s valuation. It is hard to value startups early on. Deferring the valuation until a larger equity round is raised is one way to address this (this doesn’t apply if you are using a post-money SAFE).

- they have a lower cost to execute. Convertible notes are simple and flexible. It involves a single document, whereas even small equity investments can involve a subscription agreement, shareholders’ agreement and a new constitution.

- there are fewer representations and warranties. Subscription agreements often include multiple representations and warranties which are inappropriate for an early stage startup. A convertible note generally includes only a handful of very focused warranties.

- they concede much less control. Noteholders typically receive little (if any) control over the company, e.g. no veto or director appointment rights. This works well with the need for startups to pivot and to raise the next round of funding without investor interference

- less administrative burden. The fewer shareholders you have, the less shareholder notices and other company secretarial formalities you have to deal with.

pros and cons: disadvantages of convertible notes

However, there are some downsides to convertible notes from a founder’s point of view:

- KISS convertible notes are debt. The clock starts running towards repayment on the maturity date. If you have not completed a qualifying capital raise by that date, the debt needs to be repaid. While it is uncommon for investors to enforce that right and force the winding up the company if the debt cannot be repaid, you may have to renegotiate some form of refinancing with note holders at which point you will be seriously on the back foot. However, this does not apply to SAFE notes which are quasi-equity.

- preference shares generally issued on conversion. Most convertible notes convert into the class of shares issued to the investors on the next round of financing. In Southeast Asia, this means preference shares. As a result, convertible note investors have the double protection of both a price discount on conversion, plus the liquidation preference negotiated by the subsequent investors

- detached investors. Convertible notes often don’t include information or participation rights in later financings. This means convertible note investors are not as involved in the business as they might be by owning equity. But, startups need all the help they can get, so make sure that your note holders are real supporters of the business and can potentially help bring in the next round of funding

Notes remain a very effective tool due to how quickly deals convertible note deals can be closed – we have seen convertible note financing rounds closed in Southeast Asia in a few days. For startups looking to raise money fast and get on with growing the business, this speed remains a key factor.

New to Kindrik Partners? View other resources in our series on capital raising in Southeast Asia:

introduction

In a previous guide on raising seed capital in Southeast Asia, we discussed getting investor ready, including where Southeast Asian startups should incorporate their company, founder arrangements, and group structure.

In this guide, we talk about how to structure seed investments, the key terms and documentation, and how to go about finding investors.

convertible notes

Many seed investment rounds in Southeast Asia complete using convertible note instruments like the 500 Startups Keep-It-Simple-Security (KISS). These are unsecured debt instruments that convert to equity when a company completes its next equity raising.

The KISS is the most common type of convertible note used in Southeast Asia. If you are contemplating a seed round, we suggest you upskill on this document by downloading a version of the KISS adapted for Southeast Asia from our website.

There are other forms of note in use in Southeast Asia, including US style documents. With these documents, US specific provisions need to be amended, e.g. removing US securities law and taxation language which shouldn’t be relevant for a non-US issuer.

Convertible notes anticipate that the investment amount is drawn down either in a lump sum on one date or, more likely, over a period of time. The investment amount typically automatically converts to equity on the date of a qualifying capital raise at a discounted price to the next round price, but subject to an overall valuation cap.

If not already converted, the debt may be repayable (potentially at a multiple of the outstanding amount) or convertible at the noteholder’s discretion:

- on the occurrence of a liquidity event, i.e. the sale of your company

- at the maturity date for the note. This is often at least 18 months from the initial drawdown.

Convertible notes have been successful in Southeast Asia partly due to the availability of series A money. This gives noteholders comfort that you are likely to raise follow-on capital quite quickly, which triggers conversion of the note into equity.

key features of convertible notes

| Investment Amount | The amount to be invested by the investor (noteholders) |

| Series | Notes of a particular series are issued on the same terms. Typically, you may have a period of time to issue further notes on the same terms without seeking the consent of existing noteholders. The total investment amount is sometimes drawn down in a lump sum on one date or over a period of time with multiple closings |

| Interest | This is the annual rate at which interest accrues on the note whilst it is outstanding. In Southeast Asia, the rate varies, but usually is a low amount, e.g., 1% or 2% |

| Maturity Date | This is the date on which the debt is due for repayment. This should be a reasonable period of time from the date of the note, so that the company can achieve the qualifying capital raise (see below) to trigger conversion. In Southeast Asia, periods to maturity are generally set at 18 months and can be longer. Usually, if the company is unable to raise money before maturity, the majority of noteholders can elect for the debt to convert to shares rather than demanding repayment |

| Qualifying Amount | The investment amount of the notes will automatically convert into shares at the time of the company’s next capital raise. There is normally a minimum amount that must be raised to trigger conversion (called a qualifying capital raise), which is set to ensure that the raise is a legitimate company financing, not a device to trigger conversion |

| Discount | Assuming the company’s next financing round is a qualifying financing, the notes will automatically convert into shares often at a discount to the share price paid in that financing. The discount is intended to compensate investors for the risk they take on by investing at an early stage. In Southeast Asia, this discount is typically 15-25%. This follows Silicon Valley norms |

| Valuation Cap | This addresses an initial concern that investors had with the KISS style and other convertible notes – that the company’s valuation could increase significantly and they would only have the protection of the discount to the price of the next funding round. The valuation cap effectively caps the price at which investors pay for their shares when the note converts. If your company raises a financing round at a $5 million pre-financing valuation but the convertible notes have a $2 million valuation cap, your note holders will effectively receive a 60% discount to the price that the new investors are paying. So consider a valuation cap carefully as it can have a significant dilutive effect on the next round of financing if set too low |

| Majority-in-Interest | This term simply means those noteholders holding a majority of the total investment amount of the series. It is useful to incorporate this concept into the document so that key decisions are taken, or rights waived, not by individual investors but on a majority rules basis |

convertible notes vs equity

There has been a lot written on this topic. For a founder’s take on the debate, have a look at the blog Seedinvest: Pros and Cons of Convertible Notes or 500startups KISS blog post. For an investor point of view, Jason Lemkin’s SaaStr blog post An insiders’ guide to convertible debt vs equity is good read.

From a founder’s perspective, the biggest benefit of convertible notes over an equity financing is speed. The note is generally a single document with simpler terms to negotiate, and without lots of conditions, representations and warranties. In addition, the KISS and other most convertible notes are designed to be executed by individual investors, so it is possible to receive funds without closing with all investors simultaneously.

Other benefits of convertible notes include:

- postpones the difficult discussion about the company’s valuation. It is hard to value startups early on. Deferring the valuation until a larger equity round is raised is one way to address this. Also, if a third party is prepared to invest at a particular point in time and valuation, it provides some level of market evidence of the valuation for the notes.

- lower cost to execute. Convertible notes are simple and flexible. It involves a single document, whereas even small equity investments can involve a subscription agreement, shareholders’ agreement and a new constitution

- fewer representations and warranties. Subscription agreements often include multiple representations and warranties which are inappropriate for an early stage startup. A convertible note generally includes only a handful of very focused warranties, avoiding protracted negotiations and unnecessary time spent on disclosure by the company

- concedes much less control. Noteholders typically receive little (if any) control over the company, e.g. no veto or director appointment rights. This works well with the need for startups to pivot and to raise the next round of funding without investor interference. Because notes provide this flexibility, there has been good success rate of note financed companies raising a series A follow-on round

- less administrative burden. The fewer shareholders you have, the less shareholder notices and other company secretarial formalities you have to deal with.

However, there are some downsides to convertible notes from a founder’s point of view:

- convertible notes are debt. The clock starts running towards repayment on the maturity date. If you have not completed a qualifying capital raise by that date, the debt needs to be repaid. While it is uncommon for investors to enforce that right and force the winding up the company if the debt cannot be repaid, you may have to renegotiate some form of refinancing with note holders

- preference shares generally issued on conversion. Most convertible notes convert into the class of shares issued to the investors on the next round of financing. In Southeast Asia, this means preference shares. As a result, convertible note investors have the double protection of both a price discount on conversion plus the liquidation preference negotiated by the lead follow-on investors

- disenfranchised investors. Convertible notes have valuation caps and often don’t include information or participation rights in later financings. This means convertible note investors are not as involved in the business as they might be by owning equity. But, startups need all the help they can get, so make sure that your note holders are real supporters of the business and can potentially help bring in the next round of funding

- additional protections. Finally, convertible notes can sometimes include additional protections for noteholders, such as participation rights, additional reporting from the company, and a most-favoured-nation provision (which gives noteholders comfort that they will receive a replacement convertible note if one is subsequently issued on better terms). Avoid these if possible, but if investors insist on them, ensure that they can be waived by a majority of the note holders.

Notes carry some uncertainty, particularly if follow-on money is unavailable, But in Southeast Asia, they remain a very effective tool, predominantly due to how quickly deals are closed – we have seen convertible note financing rounds closed in Southeast Asia in a few days. For startups looking to raise money fast and get on with growing the business, this remains a key factor.

seed equity financings

Convertible notes are not always an option since some investors prefer the certainty of equity even on seed rounds.

If the amount being raised is not significant then it is in everyone’s interests to keep the documentation simple and get the round closed quickly. Try to avoid “Series A” terms and documentation as this is likely to be overkill and is likely to limit your flexibility both in terms of how you grow your business and how you raise further capital.

Small seed investments can be completed using our southeast asia seed investment term sheet, subscription agreement and shareholders’ agreement.

Keep the following tips in mind:

- issue ordinary shares – as soon as companies start issuing preference shares, the deal becomes more complex with discussions on liquidation preferences, conversion mechanics, and anti-dilution rights

- aim to keep the subscription agreement (which sets outs the mechanics and terms of the investment) simple. Ideally, include only a limited set of representations and warranties covering items such as compliance with reporting obligations, IP ownership, and confirmation of no claims

- put in place only a simple shareholders’ agreement which contains fundamental rights and obligations for the governance of your company (e.g., information rights, pro-rata participation rights in future financings, and non-competes). Avoid any investor consent rights so that investors do not need to be consulted except for significant capital expenditure or a material change in the direction of the company

- avoid amending the company’s articles of association or constitution (as applicable) – this should be possible as long as you avoid issuing preference shares

- aim to have the company’s lawyer prepare the documents as this usually ensures reasonable first drafts can be presented.

corporate authorities

All seed capital raising transactions in Southeast Asia require corporate authorisations which your company secretary will need to complete.

E.g., in Singapore, directors’ and/or shareholders’ resolutions will need to cover:

- approval of all the transaction documents, including any convertible note or the subscription and shareholders’ agreements (as applicable)

- adoption of the new constitution or articles of association of the company (if required)

- the issue of the subscription shares to the investors

- the appointment of any investor director(s) to the board of directors

- an obligation on the investors to pay the subscription monies to the company’s bank account

- approval and execution of any service agreement if founders are to become executive directors of the company.

Aside from the transaction documentation, ACRA requires that Singapore based company secretaries carry out stringent know-your-client (KYC) checks on new shareholders.

You should plan for this early in the process to ensure that this investor KYC documentation does not hold up closing the deal.

finding investors

There are now over 25 active venture capital funds based out of Singapore focused on the Southeast Asia region. Many of these funds have participated in seed investment rounds as well as larger follow-on capital raisings.

Tech-in-Asia have provided a useful directory of VC firms and angel investors with a presence in Singapore that have been investing in startups in the last few years. Some of these funds were supported by the Singapore government through the National Research Foundations Technology Incubation Scheme (NRF TIS) and the Early Stage Venture Fund (ESVF). The NRF continues to evolve with the future ESVF initiatives being announced in early 2016. Further information can be found on the NRF’s website.