BLOG

7 common pitfalls for startup founders

share:

As startup lawyers, we tend to see when things go wrong for companies and their founders more often than most people. To save you having to untangle easily avoidable issues, we’ve created a list of common pitfalls for startup founders.

The good news is these issues are easy to avoid with a bit of planning.

#1 not giving love to your cap table

Your cap table needs to be accurate and mirror the formal share register. We have seen fundraising transactions postponed or even cancelled where founders have not been able to clearly explain their cap table to investors.

Warning signs that you might have a cap table issue looming:

- inaccurate cap tables not showing convertible instruments at all, or incorrectly.

- if you’ve promised options or shares to people but not clearly documented these arrangements. For example, indicating to employees that they mightget a certain percentage of the company in shares or options could end up being legally binding and yet confusing – a percentage of what and when??

how to avoid this pitfall:

Keep track of both your cap table and your share register, whether using specific software or a simple excel spreadsheet. Only allocate options under a formal share scheme approved by the board.

bonus tip: ESOPs and cap tables:

A common question we get from founders is, “how does my ESOP appear on my share register and/or my cap table?”

The answer is that options are not recorded on a company’s share register or on its public filings. However, cap tables typically include the ESOP allocation together with any other convertible instruments such as convertible notes or warrants.

This means that your current share register might differ from your fully diluted holding (i.e. after accounting for your ESOP).

#2 not having vesting arrangements in place

It is a misconception that vesting is something that only investors like to see. Vesting agreements are key from the outset: covering founders and also any advisors who are offered shares. Why? They protect your startup if founders or advisors move on quickly, by enabling the company to claw-back unvested shares.

Having a large percentage of a company’s equity held by people who are no longer contributing is not efficient – those shares could be used to incentivise others in the business, plus new hires.

what to do:

Get vesting agreements in place for founders and advisors. For founders, this should cover some, but most likely not all, of their shares. If shares are to be issued to advisors up front for future services, the company needs a mechanism to buy back some or all of those shares, not just if the advisor leaves, but also if they don’t deliver what was expected.

#3 signing the term sheet without negotiation

Most of the tricky legal and commercial issues are set out in the term sheet. Whilst term sheets are usually legally non-binding it is important to negotiate them with the help of a lawyer before signing. It is difficult to get investors to go back on what was already agreed.

what to do:

Engage a lawyer at term sheet stage. An experienced startup and VC lawyer can review and provide comments on a term sheet in under a couple of hours. This is a good investment if, as in most cases, it helps you secure more balanced documents and deal terms.

bonus tip: short form term sheets:

Be wary of short form term sheets that appear to leave all the key issues to the long form transaction documents. Whilst you’ll probably sign this kind of term sheet quickly – the likelihood is you are simply delaying the real discussions until later. If there are investor friendly deal terms you’ll want to know early on in the process so you don’t waste time, and then not proceed with the deal. Check out our video guide on negotiating a series A term sheet.

#4 underestimating the time taken to fundraise

Documents are becoming standardised and financing rounds closing more quickly. That said, the process always takes longer than founders think. Series A rounds can take 3 months from signing the term sheet, especially where there are lots of moving parts (e.g. if you have a lot of investors to deal with, or several existing shareholders).

Founders sometimes get deal weary at the end of a long process and concede material points just to get it over the line. Therefore, have realistic expectations on timeframe from the outset and, if necessary, start the fundraising process sooner if cash flow is tight.

how you can minimise the fundraising timeframe:

- start early.

- get organised. Set up and maintain an electronic due diligence folder (sometimes called a data room) before you’ve started the fundraising process. This should contain all your indexed company documents, records and signed agreements.

- don’t leave the disclosure process until the last minute on a fundraising transaction – disclosure is critical to protect the company and founders against claims by investors.

- use a completion checklist to streamline the closing process.

#5 making everything too complex

Speed and simplicity often carries the day. Startups can go wrong when they make things complex, especially when it comes to fundraising.

warning signs:

If the convertible note you are negotiating is now 20 pages or more, you’ve probably defeated the purpose of using a note in the first place.

If you are raising a very small funding round but the investment is only drawn down in tranches and/or involves KPIs, you might well be speaking to the wrong investors.

how you can avoid this:

- take the easy route where you can. Use standardised terms for convertible notes like the KISS but check with your lawyer on the terms – they can point out quickly the key points to negotiate (if any).

- work with good series A templates such as the Singapore VIMA model documents and don’t try to reinvent the wheel.

- raise a little less money if you can do so much more quickly on simpler terms.

#6 agreeing to harsh terms with early investors because you need the cash

Conceding material issues in early seed rounds can set a precedent in future fundraisings. It’s not the type of thing that you can ‘fix’ down the road.

For example, if your first round of investors end up with a 2x participating liquidation preference (which would not be considered to be market standard), your future investors are likely to ask for the same, or worse. This becomes more material as the funding rounds “stack” on top of each other of course.

The same applies on control rights. For example requiring all investors to approve certain board matters (rather than a majority) is inefficient, and may encourage future investors to ask for the same (ending up in approval gridlock).

how you can avoid this:

Think about the next round when you are negotiating the current one. Stick to market standards and spend time negotiating the key economic and control rights rather than issues that make little difference to your end goals.

#7 letting your record keeping lapse

Bad record keeping will cost you time, money and aggravation down the line and make you look disorganised when talking to investors.

Depending on where your startup is incorporated, you will have certain statutory and filing requirements. In some countries (such as Singapore), you may have a company secretary who helps you with this.

Startups move quickly. One minute your company has a few ordinary shares held by a couple of founders, and before you know it there are investors, several classes of preference shares, convertible notes and an ESOP.

what you can do to make it easier:

- work with a company secretarial firm that understands the dynamic startup environment so that the paperwork approving transactions and matters can be prepared quickly. Some company secretaries now offer to keep all necessary files on an online platform for easy house-keeping.

- ensure all signed documents are stored in electronic files and updated regularly. This will speed up the process when distributing information to investors.

need a hand? If any of this raises questions for you, we’re happy to help you out. Book a time with one of our startup lawyers and get a 30 minute free consultation.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

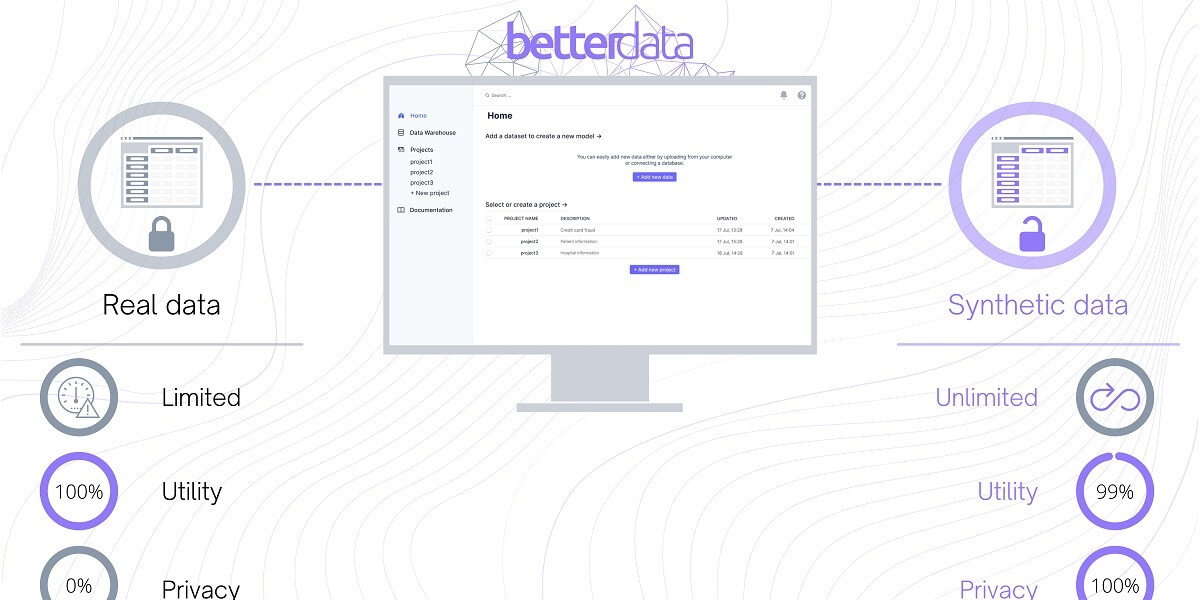

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.