BLOG

Updated Singapore model VC documents

share:

The template documents used in the venture capital ecosystem across Southeast Asia have been updated. Launched by the Singapore Academy of Law and the Singapore Venture & Private Capital Association in 2018, the new VIMA 2.0 documents are available for free to help start-ups.

8 new documents have been added to the suite of documents, including a founders’ agreement, a model constitution, an IP assignment, and an employee share option plan primer. The inclusion of a template letter covering Environmental, Social and Governance (ESG) matters reflects the increasing trend of investors to seek ESG commitments from their portfolio companies.

The core investment documents from 2018 have also been updated. This includes the two term sheet forms, the subscription agreement, and the shareholders’ agreement. We’ve summarised the main changes to these documents below (note this is non-exhaustive).

Term sheet (short form)

- clarifies that all parties bear their own costs

- provides that no dividends are to be paid to ordinary shareholders unless the holders of the preference shares either first or simultaneously receive a pro rata share of such dividends

- provides an option for the liquidation preference to be a multiple of original investment funds

- makes completion subject to customary conditions precedent

- expands the representations and warranties, including providing a general indemnity

- adds the option for pre-emptive rights to be provided to shareholders holding a certain percentage of shares

Term sheet (long form)

All changes made to the short form term sheet, plus it:

- adds clarification to the liquidation preference provision requiring that, if available proceeds are insufficient to make payments in full to preference shareholders on a liquidity event, the proceeds be shared among the holders of preference shares pro rata on an as-converted basis

- adds an optional provision to prohibit variation of the shareholders’ agreement unless agreed by all parties or by a certain % of shareholders

- lists certain new conditions precedent

Subscription agreement

- adds new default conditions precedent (clause 2 and schedule 4)

- includes new pre-completion undertakings (clause 3)

- changes the completion mechanics (clause 4.1)

- adds provisions detailing what happens if a single investor or the company fails to perform its obligations on completion – e.g., whether completion can occur with the other investors or not (clauses 4.4 and 4.5)

- adds a founder specific cap on liability (clause 8.4)

- allows an investor to assign or transfer its rights, benefits, interests and/or obligations to an affiliate

- adds new warranties covering items such as anti-money laundering, IP assignment by employees, and insolvency (schedule 6)

- includes a disclosure schedule that removes the need for a separate disclosure letter (schedule 8)

- removes the terms and conditions of the preference shares

Shareholders’ agreement

- adds further provisions governing meetings and shareholders (clause 3.2)

- adds vesting provisions covering good leaver and bad leaver scenarios (clause 16)

- limits the personal liability of the founders (clause 19)

- expands the termination provision so that it automatically terminates in certain situations (e.g. on an IPO). Termination does not release a party from accrued rights, obligations and liabilities (clause 21)

- adds a new schedule including the terms and conditions of the preference shares (schedule 3).

Round up

The amendments reflect changes commonly made by lawyers who use them on deals, and overall are an improvement. E.g., the new conditions precedent included in the subscription agreement are customary for equity financing transactions. The better place for the terms and conditions of the preference shares was arguably always in the shareholders’ agreement, as it is now. Including founder vesting provisions, caps on founder personal liability, and anti-corruption warranties/undertakings really just reflects market practice. The move to a disclosure schedule is also a good idea to remove the need for a separate letter.

There were some improvements that were missed. E.g., the tag along formula still does not reflect most tag along/co-sale provisions that we see in the market; and the liquidation preference language continues to require an actual conversion into ordinary shares (assuming proceeds come out higher on an as-converted basis), which would be avoided with more conventional drafting.

explore our other blog posts

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

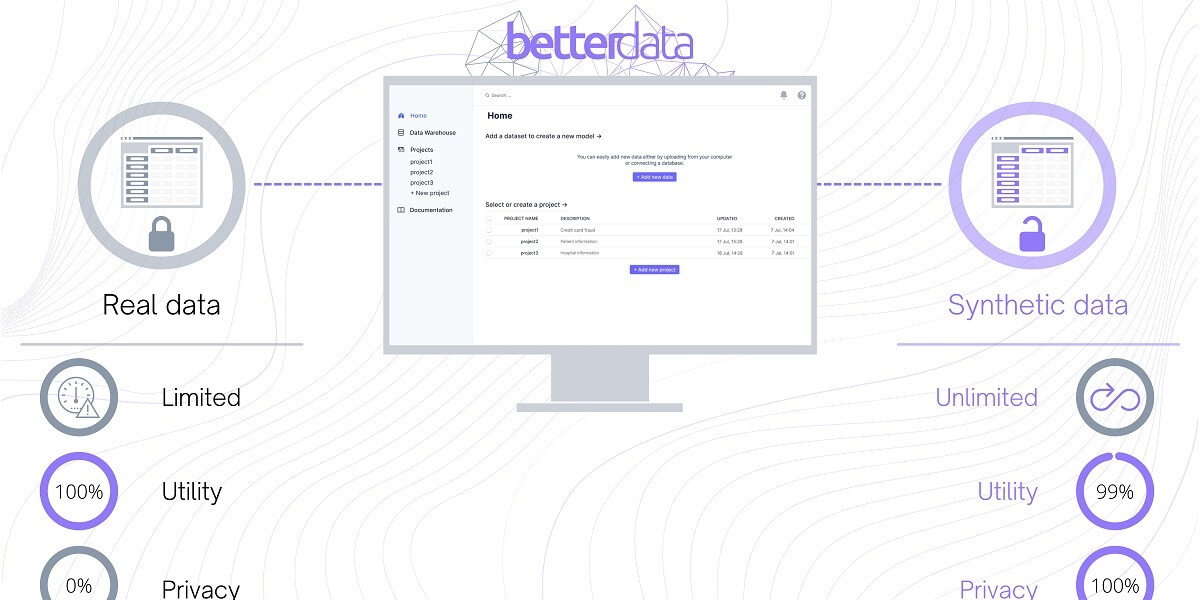

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.