free legal templates

all of our legal templates are free, forever

search our resources

legal templates for startups in southeast asia

starting out? start here

Save time and money on legal fees with our free legal templates for routine legal paperwork, tailored to the Southeast Asian market.

made for cash-strapped startups

Our aim is to empower startups to self-serve their legal basics. Browse our documents, download what you need, and save your legal spend for the things that really matter.

available for template questions

If you need to talk, just get in touch and speak to one of our startup lawyers in Singapore.

working with the hottest tech startups in southeast asia

using our templates

Our library of awesome free legal templates is available for use by business users, including legal services providers. You can download, use and modify the templates free of charge subject to our template terms of use.

Click on any template below to access it. You will be given the choice of downloading a PDF version of the template or an editable Word version.

get a lawyer to review your work

The templates are a guide only. You are welcome to use them, but because of their nature, we have had to make them generic. They do not cater for every situation.

Businesses using the templates will need to consult their lawyer to ensure that their use of these documents is appropriate to their situation.

filter by category

This agreement is for use when a company primarily wishes to bring in employees from a target company, rather than acquiring its business. Acqui-hires are common amongst well-funded startups looking to expand their teams by hiring talent from other startups. Often the employees are acqui-hired from businesses that are failing and are subsequently shut down.

This agreement covers the transfer of the employees and release of any existing restraints, together with a general assignment of intellectual property rights. It sets out the terms of payment of the acquisition amount – this is sometimes paid in tranches and adjusted if the transferring employees subsequently move on soon after completion of the acqui-hire.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple agreement for the provision of advisory services to an early stage company (including where a company is establishing a formal advisory board).

This template is drafted on the basis that the advisor is to receive shares in the company as compensation for the services provided. It assumes no cash compensation will be paid. Some of the shares may be clawed back by the company if the advisor fails to make the expected contributions over the agreed period, which is usually one or two years.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This template cap table is intended for use when considering a potential equity investment in a company (whether from existing shareholders, external investors, or both). The template works when the number of new shares to be issued is calculated:

- based on a specific investment amount at a specific pre-money valuation of the company e.g. an aggregate investment of $500,000 at a pre-money valuation of $2m

- on a fully diluted basis i.e. all unexercised options (if any) are treated as existing shares in the company for the purpose of calculating the number of new shares to be issued

- no anti-dilution rights are triggered by the issue of the new shares

- all shares issued in consideration for the conversion of debt to equity are issued at a discount to the price per share paid by the cash investors. If all of the debt is converting at the same price per share paid by the cash investors please use our template investment capitalisation table for debt converting without a discount

- the investment is made on a fully diluted basis, i.e. if a new employee share option plan (ESOP) is established as part of the investment round, the dilutionary effect of the ESOP is borne entirely by the founders and any other existing shareholders, and not by the investors. This is the most common approach.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This template cap table is intended for use when considering a potential equity investment in a company (whether from existing shareholders, external investors, or both). The template works when the number of new shares to be issued is calculated:

- based on a specific investment amount at a specific pre-money valuation of the company e.g. an aggregate investment of $500,000 at a pre-money valuation of $2m

- on a fully diluted basis i.e. all unexercised options (if any) are treated as existing shares in the company for the purpose of calculating the number of new shares to be issued

- no anti-dilution rights are triggered by the issue of the new shares

- all of the new shares are issued at the same price per share, including any new shares issued in consideration for the conversion of debt to equity. If all of the debt is converting at a discount to the price per share paid by the cash investors (e.g. under the terms of an existing convertible loan agreement) please use our template investment capitalisation table for debt converting at a discount.

- the investment is made on a fully diluted basis, i.e. if a new employee share option plan (ESOP) is established as part of the investment round, the dilutionary effect of the ESOP is borne entirely by the founders and any other existing shareholders, and not by the investors. This is the most common approach.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This Due Diligence Document List is a list of legal documents for review by potential investors. Investors are likely to request additional documents, depending on the nature of the company’s business, but this list is a good starting point.

We suggest that companies keep an electronic file of the documents in this list so that when requested, they can be provided quickly. In any event, once you begin to consider raising capital, an early task will be to gather the documents set out in this document list.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a template checklist which sets out the steps typically required to take a series A investment transaction from signing to completion. The items included are examples only; when creating your own checklist you should always refer to the key transaction documents (typically a subscription agreement and shareholders’ agreement, and a new constitution reflecting the terms of the shareholders’ agreement) to determine what items need completing.

As this checklist covers only the most typical completion steps, it does not provide for the following items which are sometimes seen on investment transactions:

- a rolling close, under which the company has a set amount of time after completion to find investment from other investors on the same terms

- investment in tranches, i.e. more than one closing date

- conversion of any debt or convertible notes on completion of the investment.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

what this is

This note is a convertible instrument that is intended to be used by a startup to document a seed investment from a third party investor or a bridge financing from existing shareholders.

The terms of the note are substantially based on the keep-it-simple-security created by 500 Startups and include some of the investor friendly provisions typically included in convertible seed investments in the US and as adopted for other global markets.

how it works

This note anticipates that the investment amount is drawn down in one lump sum and is unsecured. The investment amount:

- automatically converts to equity on the date of a qualifying capital raise

- is repayable (potentially at a multiple of the outstanding amount) or convertible at the investor’s discretion on the occurrence of a liquidity event

- is repayable or convertible at the investor’s discretion at any time following maturity.

This note also anticipates that it may be one of a series of identical notes entered into as part of a seed investment round. In that case, some decisions that relate to the investment round as a whole are to be made by a majority of the investors, rather than by an individual investor.

related guides

- 8 key features of convertible notes in southeast asia

- raising capital for your startup: convertible notes vs equity

- raising seed capital in southeast asia: structure & terms

you might also like

We also have another popular variation of the convertible note – our SAFE convertible note template.

The terms of the note are substantially based on the simple agreement for future equity created by the US accelerator, Y-Combinator.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple term sheet for a convertible instrument that is intended to be used by a startup to document a seed investment from a third party investor or a bridge financing from existing shareholders.

The terms of the note are substantially based on the keep-it-simple-security (KISS) created by 500 Startups and include some of the investor friendly provisions typically included in convertible seed investments in the US and as adopted for other global markets.This term sheet anticipates that the investment amount is drawn down in one lump sum and is unsecured. The investment amount:

- automatically converts to equity on the date of a qualifying capital raise

- is repayable (potentially at a multiple of the outstanding amount) or convertible at the investor’s discretion on the occurrence of a liquidity event

- is repayable or convertible at the investor’s discretion at any time following maturity.

This term sheet also anticipates that it may be one of a series of identical notes entered into as part of a seed investment round. In that case, some decisions that relate to the investment round as a whole are to be made by a majority of the investors, rather than by an individual investor.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a template disclosure letter for disclosing against warranties provided in an M&A or capital raising transaction.

read our guide: tricky clauses: warranty disclosures (4 minute read)

read our guide: raising seed capital in southeast asia (8 minute read)

Typically under these transactions, a company (and, in some cases, its founders) provides statements to a purchaser or investor in the transaction documents. If any of these statements (known as warranties) turn out to be untrue, the purchaser or investor can bring a claim for a breach and potentially recover money from the parties that gave the warranties.

A disclosure letter protects warrantors, by allowing them to disclose any matters that are inconsistent with the warranties set out in the transaction documents. The purchaser or investor cannot bring a warranty claim in respect of matters which have been fairly disclosed. The disclosure letter is the document which formally records these disclosed exceptions to the warranties. It is therefore an integral part of the transaction documents and the earlier warrantors start preparing the document on any transaction, the better.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This document is intended for use by the founders of a new startup who wish to provide for some level of claw-back of a co-founder’s initial shareholding if he or she:

- ceases to work for the company (whether as an employee or contractor); or

- fails to make the contribution required of them to the business.

This type of arrangement is referred to in the startup and venture capital world as founder vesting.

The approach taken in this document is to provide for progressive vesting of a co-founder’s shares over a set period (e.g. 36 months). If the co-founder leaves the company or fails to make the required contribution to the business during that period, the company has the option to repurchase unvested shares for the price originally paid by the co-founder for those shares (which will usually be nil, if the shares were issued on incorporation of the company).

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This document is a short form co-founder agreement intended for use by the founders of a new startup who wish to provide for some level of claw-back of a co-founder’s initial shareholding if he or she ceases to work for the company (whether as an employee or contractor). In this document, the company’s right to purchase shares is limited to a situation where the co-founder ceases to work for the company, i.e. there is no expected contribution from the co-founder. If you would like the company to be able to repurchase shares for a failure by the co-founder to contribute to the company, use our southeast asia co-founder agreement – long form.

This type of arrangement is referred to in the startup and venture capital world as founder vesting.

The approach taken in this document is to provide for progressive vesting of a co-founder’s shares over a set period (e.g. 36 months). If the co-founder leaves the company during that period, the company has the option to repurchase unvested shares for the price originally paid by the co-founder for those shares (which will usually be nil, if the shares were issued on incorporation of the company).

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This agreement is for use when a startup wishes to issue shares to a new investor as part of a friends and family investment round in Southeast Asia. It sets out the mechanics for the investment and the warranties to be given by the startup. It provides for investment for ordinary shares in the company in one tranche, with no conditions (other than those relating to corporate authorisations).

There are no standard terms that apply to investment by friends and family type investors – these types of investments can often be relatively informal and may not always include the investor protection provisions required by professional investors or formal investment groups, such as angel groups.

Your lawyer or company secretary will need to complete any necessary board and/or shareholder resolutions needed to implement this document.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple company friendly consultancy agreement for engaging independent contractors or consultants (e.g. individuals or sole operator companies) to work within a business.

This template includes a restraint on the independent contractor to ensure that the independent contractor does not jeopardise the company’s business (by competing or similar) during the term and for a set period after. To be enforceable, a restraint must be reasonable. This, in turn, will depend on the facts relating to the agreement. However, the longer the restraint and the broader the restrained area, the more likely that arguments could be raised about the enforceability of the restraint.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

Technology businesses in Southeast Asia often have group structures. For example, a business may have trading subsidiaries in Indonesia, Malaysia and/or the Philippines, and a holding company in Singapore. Loan arrangements within such group structures are relatively common.

This is a simple intercompany loan agreement that records an unsecured loan between group companies.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This document is intended for use by the founders of a startup company to formally transfer intellectual property relevant to the business, products or services of the company, to that company.

Before completing this deed, we suggest that companies and their founders first work to identify and record the intellectual property that the company intends to use (or is already using) in its business, including details of who:

- created the intellectual property, and on what basis (e.g. as a founder, employee or external consultant of the company)

- owns that intellectual property and on what basis (i.e. if the company owns intellectual property because it was created by its employees in the course of their employment, this should be recorded)

This will help:

- to identify intellectual property that needs to be transferred by a founder or consultant, etc. to the company (and to properly describe that intellectual property in a deed of assignment)

- to prove ownership of the company’s intellectual property in the future, e.g. in a capital raising or M&A transaction.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple document to outline the main in principle terms of a proposed commercial relationship. The document is not legally binding (other than the confidentiality, termination, and governing law provisions in part D).

Other than the statement that the document is not intended to be binding and part D, there is no suggested content included – the document is simply a framework for the parties to record the in principle commercial terms that have been agreed, prior to preparing a formal agreement.

Although the letter of intent is non-binding, it can create moral or ethical obligations that are difficult to back away from. It is therefore important not to over-promise, and to set out relevant assumptions.

This document does not include an exclusivity provision – either party is free to enter into negotiations, or contract, with third parties for a similar or competing relationship.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This Due Diligence Document List is a list of legal documents for review by potential purchasers of the shares or assets of a target company in a private M&A transaction. In the course of the purchaser’s due diligence investigations, additional questions will inevitably arise, but this list is a good starting point.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a template term sheet for use when one tech company is acquiring the shares of another tech company. It sets out the principal terms agreed between the acquiring company and the shareholders of the target company prior to preparing the formal sale and purchase agreement. The acquisition of a competing and/or complementary business in this manner is a common strategy of well-funded high growth technology companies.

This term sheet assumes that the transaction will be structured as a share sale (as is most common). It should not be used in connection with an acquisition of the business and assets of a target company. This term sheet is not legally binding (other than the confidentiality obligations in part B); it simply sets out the terms agreed in relation to the acquisition.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple mutual (or two way) confidentiality agreement setting out the terms on which each party will keep confidential the other party’s information.

It has been drafted to be fair to both parties and to enable easy signing (without the need for lengthy negotiation). If the purpose for which the information is being exchanged is highly sensitive or has unique aspects, consider whether a more belts and braces agreement may be required.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

what this is

This note is a convertible instrument that is intended to be used to document a seed investment from a third-party investor or a bridge financing from existing shareholders.

The terms of the note are substantially based on the simple agreement for future equity created by the US accelerator, Y-Combinator.

how it works

This agreement anticipates that the investment amount is drawn down in a lump sum on one date and is unsecured. The amount of the investment is not a loan, has no set maturity or repayment date and does not accrue interest. The investment amount remains outstanding until:

- it is automatically converted to equity on the date of a qualifying equity financing

- it is repaid or converted (at the election of the investor) on the occurrence of a liquidity event.

related guides

- 8 key features of convertible notes in southeast asia

- raising capital for your startup: convertible notes vs equity

- raising seed capital in southeast asia: structure & terms

you might also like

We also have another popular variation of the convertible note – our KISS convertible note template.

The terms of the note are substantially based on the keep-it-simple-security created by 500 Startups.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple term sheet for use when a startup is raising capital from seed investors in Southeast Asia. It sets out the terms agreed between the company and the investors prior to preparing the formal agreements. Generally in this type of capital raising the formal agreements will be a subscription agreement – see the template southeast asia seed subscription agreement – and a shareholders’ agreement – see the template southeast asia seed shareholders’ agreement. The term sheet is not legally binding (other than the confidentiality obligations in part B); it simply sets out the terms agreed in relation to an investment.

There are no standard terms that apply to investment by seed investors – these types of investments can often be relatively informal and may not always include the investor protection provisions required by professional investors on larger series A investment rounds. We recommend that you read our guides to raising seed capital in southeast asia.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple shareholders’ agreement intended to be implemented by a startup at the time it closes a seed investment round in Southeast Asia.

This agreement deals with the management of the startup and the relationship between the founders, any other existing shareholders and the investors (e.g. rights to appoint directors, matters requiring the approval of any investor-appointed directors, the provision of financial information, confidentiality provisions, etc).

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This agreement is for use when a startup wishes to issue shares to a new investor as part of a seed investment round in Southeast Asia. It sets out the mechanics for the investment and the warranties to be given by the startup. It provides for investment for ordinary shares in the company in one tranche, with no conditions (other than those relating to corporate authorisations).

There are no standard terms that apply to investment by seed investors – these types of investments can often be relatively informal and may not always include the investor protection provisions required by professional investors on larger series A investment rounds.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a term sheet for use when a startup based in Southeast Asia is raising capital from series A investors. It sets out the terms agreed between the startup and the investors prior to preparing the formal agreements. Generally in this type of capital raising the formal agreements will be a subscription agreement, a shareholders’ agreement and an updated constitution. The term sheet is not legally binding (other than the confidentiality and exclusivity obligations in part B); it simply sets out the terms agreed in relation to an investment.

There are no standard terms that apply to investment from series A investors in Southeast Asia. We recommend that you read our guides to raising series A capital in southeast asia.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This agreement is for use by Southeast Asian companies looking to redomicile or flip to Singapore. Our experience is that, with a few exceptions, most Southeast Asian tech startups wishing to raise capital from professional investors end up being domiciled in Singapore (either to attract investment or as a requirement of their investors).

Flipping to a new jurisdiction can be done in two ways: either by a transfer of shares or by a transfer of assets. Please see our guides to raising seed capital in southeast asia for more information on the different processes involved. This agreement is for the first option – where the shares in your existing company are transferred to a newly incorporated Singapore company. That new company then issues shares to the shareholders of the existing company in equal proportions. These are separate corporate transactions in two different jurisdictions requiring legal and tax advice in each of those jurisdictions.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

This is a simple startup shareholders’ agreement for use during the earliest stage of a company’s development, i.e. while the founders are the only shareholders and before the company receives funding.

This agreement is intended to cover matters that are often important to founders but that are not always covered in off-the-shelf company constitutions, specifically:

- the composition of the board

- pre-emptive rights on new share issues

- rights of first refusal on transfers of existing shares

- non-compete undertakings

- assignment of intellectual property rights.

using our templates

Use of a template by business users is free of charge and is subject to you agreeing to our template terms of use.

From capital raisings to drafting governance contracts, we help startups every day with their legal needs. We’ve created a new guide to help founders find their feet: Top Ten Legal Templates for Startups: A guide for companies based in Southeast Asia.

This guide contains basic tips when putting this paperwork in place. Having these documents in order can help your startup further down the line, particularly when raising investment. With each template, we cover what it does, when a startup might need to use it, and essential points that founders should wrap their heads around.

All legal agreements we cover in the guide are also available for download free on our website. These templates include explanatory notes to help founders and non-lawyers complete the agreement.

Have questions about our guide or one of the templates? Feel free to get in touch with us if you’d like some help adapting one of the agreements we’ve recommended.

Access the guide by filling out your details below:

read our startup case studies

Singapore based property startup 99.co likes a challenge. Dominated by well funded regional players, there would be easier sectors to disrupt than online property. However 99.co is fighting hard with a unique proposition. The company has raised two rounds of funding since incorporation and is backed by high-profile investors including Sequoia Capital and Facebook co-founder, Eduardo Saverin.

Founder and CEO, Darius Cheung, talked to us about the company’s progress, its most recent capital raising transaction in 2015, and how they have found working with Kindrik Partners.

the 99.co story

Darius is one of Singapore’s celebrated young tech entrepreneurs having sold mobile security startup tenCube to McAfee in 2010. This was a decent sized exit for a Singapore tech startup at the time. With the current hot funding environment and massive interest in mobile disruptive technologies in Southeast Asia, Darius is now looking to build a company for an even larger exit.

Not surprisingly, given the city state’s rapid growth, Singaporeans have always had a real interest in property. So 99.co is playing in a compelling space. Singapore has over 30,000 property agents many of which use online real estate platforms such as 99.co. The company recently set up an Indonesian website and plan to get going in Malaysia and Thailand further down the line.

99.co differentiates itself from larger competitors by promising a more intuitive search experience, where the rankings for listings are influenced by the quality of the published content. The site, for example, could favour listings with more photos or with value add information such as commute times or local amenities. This contrasts with the traditional model where the level of fees paid typically pushes classifieds higher. Darius believes that users will increasingly seek this kind of consumer friendly experience.

99.co charges agents a basic subscription fee to list their properties. The company has, however, recently launched a new product called 99PRO – a subscription model where agents can unlock additional features like interactive map searches and new data.

challenges

Darius agrees that the competition is tough to crack in Singapore and the region, given the dominant players. Content is king – the number of listings is fundamental to the success of the business. Bridging the gap, and chasing the platforms that have the majority market share, requires innovative offerings. Plus it’s a crowded market. Aside from other startups trying to challenge those established players, print media still retains a surprisingly sizeable chunk of the market.

The nature of 99.co’s subscription model means the company will need to add alternative revenue streams over time.

Finally, talent acquisition in Singapore and building the 99.co team has been difficult given the number of other startups also hiring sought-after developers.

working with kindrik partners

Lee Bagshaw was introduced to Darius by one of 99.co’s investors. Lee has helped the company through each of its financing transactions. Most recently in 2015, Lee, supported by Chris Wilson, advised on the company’s series B transaction led by Sequoia and Saverin.

Darius’ previous view on lawyers had been that they were expensive and it was not always easy to see their value. He describes working with Lee as a breath of fresh air. Whether by email, on the phone, by WhatsApp or even in the passenger seat of Darius’ car, Lee’s advice was always simple to understand, but with real value add.

Darius was impressed with Kindrik Partners’s knowledge of VC financing deals in Southeast Asia. He says Lee and the team were also very fast, generally turning documents around in under 24 hours. Darius believes that, by working for a tech focussed firm, the Kindrik Partners lawyers have a greater connection with startup founders, combined with unique experience. Throughout the negotiations, Darius found that even if the company could not secure the best outcome on all points, Lee and Chris ensured that he understood clearly the implications, so he could quickly move on.

summing up

99.co are operating in an exciting space in Southeast Asia. Real estate tech companies globally have grown rapidly, achieving some astonishing valuations.

Sequoia’s and Saverin’s backing shows that notable investors are looking carefully at this space in Southeast Asia, particularly for platforms that are distinguishable from the others.

Kindrik Partners will be closely watching 99.co continue its growth to become a significant online property player in Southeast Asia.

Explore 99.co.

[Note: The firm’s name was changed to Kindrik Partners in July 2020 and references to the firm’s previous name have been updated.]

Singapore-based Pixibo provides personalised size and fit recommendations in real time for online retailers and their customers. The fashion-tech startup worked with Kindrik Partners on their recent series A raise.

We spoke to founder and CEO Rohit Kumar on Pixibo, the capital raising journey, and working with Kindrik Partners.

pixibo’s story

Rohit is an ex-Googler with experience across Europe and India, before heading to Singapore to head up operations for e-commerce advertising company Sociomantic. Between 2013 and early 2016 he launched and managed all of Sociomantic’s APAC operations and was part of the team that sold the business to dunnhumby, a Tesco company.

It was at Sociomantic that Rohit identified an issue plaguing fashion e-commerce sites. People were browsing clothes online, but very few of those visits converted into sales. “The average conversion rate is 1.5%”, says Rohit.

Pixibo’s technology was formally launched in 2018, after a few years in development. The platform makes real-time size recommendations, personalised for every shopper and for every brand and SKU. For a retailer this boosts conversion rates, reduces return rate and improves customer satisfaction. Its size recommendation engine is entirely white labelled and can be natively integrated into online stores.

“In online shopping, there’s a lot of pain points, from finding something you like, to working out which size is correct for you,” says Rohit.

“Decision fatigue can come in, reducing sales and resulting in increased return rates. The Pixibo platform works to reduce the friction felt by the consumer and the retailer.”

working with kindrik partners

“I was educating myself about series A rounds when I came across Kindrik Partners’s content online,” Rohit says.

“It was my first time doing an institutional round so I was spending more time online trying to get my head around the legal terminology and the types of things that show up. Drag alongs, tag alongs, liquidation preference clauses. There’s a lot to understand.”

(confused? see our startup glossary )

“It looked like Kindrik Partners were the best lawyers for startups,” says Rohit.

“It was clear from the content that was available online that it was their area of expertise. When I eventually needed to bring in a lawyer to help with my round, I reached out.”

on the series A round

Pixibo already had several angel investors prior to their series A round in 2018, but the startup did not have any VCs on board, so the experience was new.

“We had VPs from Google who invested at an early stage, as well as strong private angel investors. But this was the first institutional round, and it felt very different.”

A big learning was how much longer the process took. “I thought you’d just go out to market, pitch, and then get them to sign. I eventually came to understand the level of process that institutional investors require, and how this stretches out the timeline.”

“There’s a great level of detail required. From investor interest to the term sheet to drafting the shareholder’s agreement, share subscription agreement and the whole nine yards, to signing, to getting money in the bank… it can take a long time!”

Fortunately, runway was less of a concern for Pixibo. “We weren’t in a rush. We had revenue, so there was no immediate need to get funding in”, says Rohit. “We already had a recurring revenue from our licence fees we were charging. That started conversations for us with investors, too.”

working with kindrik partners

Rohit found working with Kindrik Partners and partner Lee Bagshaw provided a lot of value during the capital raising process.

“Working with Lee was great. He was very responsive to my requests and concerns and was always happy to get on a call if need be to walk through things with me.”

Kindrik Partners’s experience in capital raising in Southeast Asia was also an asset to Pixibo.

“As a first time founder, sometimes you’re like wait, hang on, why is that in there? Lee was invaluable in these situations. He understood what terms were negotiable and what terms weren’t, and was instrumental during all of the back and forth with investors.”

tips for founders embarking on their A round

Rohit has a few tips for those entrepreneurs who are considering going out to do their series A round.

- start out 6 -8 months before you need the capital: especially if it’s your first institutional round (it gets easier with a follow-on round, because you’ll have existing investors to help you get your foot in the door).

- consider a rolling close: since you’re looking for investors who are the right fit in a long-term partnership, having a rolling close allowed Pixibo to get the money in the bank from the investors who were committed, while continuing to find the perfect fit to close out our round.

- beware the temptation to think that any money will do: in the beginning, the temptation is to look for anyone with a cheque book, but then you get smarter. Find the VC’s thesis and their sweet spot, and get smarter at looking at their portfolio to see if you fit in. Who will be interested in your story?

- don’t raise too soon: Traction is important. Wait until you’re in a strong position to raise, if you can. In our case, as we’re B2B, we had clear proof points that our product works, solves a real problem for online retailers and that they are willing to pay us for it. Investors will want to see that you have put in the hard work and that capital will accelerate growth.

- have a plan for the money. You have to articulate why you need capital now, and how it will help your business.

what’s to come for pixibo

The future is bright for Pixibo, and Rohit is looking ahead to expand into new markets. “The most exciting thing about us is that we’re location agnostic. The problems retailers have in Singapore are the same ones that they have in Sydney. The opportunity is massive.”

[Note: The firm’s name was changed to Kindrik Partners in July 2020 and references to the firm’s previous name have been updated.]

Bambu is a Singapore-based robo-advisory startup. We talked to the company about working with Kindrik Partners through their successful Series A and B rounds.

bambu

Bambu is a B2B robo-advisor platform provider to banks and other financial institutions. Their digital platform allows these financial institutions to offer automated and technology-augmented investment services to their customers. The company started up in August 2016, and now has 70 staff with clients in America, Europe, the Middle East, and across Asia.

Bambu raised US$10m in their series B round which closed in June 2019. We spoke to their CEO and co-founder Ned Phillips about the fundraising process.

getting introduced to Kindrik Partners

Ned first heard about Kindrik Partners through an early investor and advisor to Bambu. When it came time to do their Series A round, Bambu had secured its first strategic investor, Franklin Templeton Investments, as well as its first venture capital investor, Wavemaker Partners. Since it was their first equity round, Ned knew it was time to bring in professional legal advisors.

As part of their search, Ned said that he met with a few of the bigger law firms, but none of them quite fit.

“You meet the partner”, he said, “but you know you’re not going to get the partner – the actual work always gets handed off to someone else in the firm.”

Kindrik Partners was transparent and honest when presenting their team. “What I liked about Kindrik Partners was that when I met Chris [Wilson] and Sarah [Yen], they said ‘this is us, you’re going to be working with us’, which was nice.“

“That made a big difference.”, says Ned. “It was important for us to know who we were dealing with, and it was very clear that it was them – that this was my team.”

raising the series a, then the series b

The series A round was very different from the seed round for Bambu. “The series A was the first time we were introduced to equity documents”, recalls Ned. “In our seed round we had used a SAFE convertible note, so there were no equity investors at that point.”

It was a big learning curve, particularly as a first-time founder. “My clearest memory about the Series A was the amount I learned about things I never knew about”, says Ned.

“There were a lot of things about equity documents that I wasn’t familiar with – tag-alongs, drag-alongs, founder vesting, liquidity preferences, warranties.”

(Unfamiliar with these terms? Click through to our startup glossary to learn more.)

When it came time for the series B round, Ned thinks that they were fortunate with how things went, and that it felt easier, attributing it to understanding more of the process and jargon.

“We had Franklin as a returning investor who was also willing to lead the round for us. We ended up with two investors filling the round – but it turned out that as soon as our round was full, everyone else wanted to come in, which was a nice problem to have.”

For other startups looking to raise money, Ned advises perseverance. “It’s not that it’s a numbers game, but it does take persistence. We reached out to so many investors. Many people give up at 10, or 20, 30, 40 people telling them no. But don’t be deterred – be polite, say thank you, and move on.”

working with Kindrik Partners

Ned describes the team as super helpful. “When we were first introduced, the fundraising process was new to me – the combination of Chris and Sarah on board to help was invaluable.”

Ned highlights Chris as an incredibly founder-friendly lawyer. “As a founder, you want to keep good investor relations, since it’s going to be a long-term relationship.”

“Chris could be the bad cop when he felt it was in the company’s best interests. He was also great at explaining what was important and what we could let go. He was strong, but fair.”

Ned also emphasises the complexity in negotiating a series A round. “Raising money isn’t just a negotiation on value (that part is done fairly quickly). There are all of these other things to decide in terms of what to hold onto and what to let go of.”

Ned recommends the law firm to other startup founders doing who are looking to raise funds for their company. “The team at Kindrik Partners really focuses on raising funds, and it’s so valuable to be talking directly with the people who are holding the pen on the documents, rather than just being a part of the sausage mill.”

“Put it this way – when it came time to do our series B, we didn’t spend one second thinking about using someone else. It was like, OK, we’re doing our round. Let’s get in touch with Kindrik Partners and get started.”

what’s next for bambu

It’s an exciting time for Bambu. The startup has lots of plans from the proceeds of their series B, including new products set for release and building their London presence. But Singapore remains home for the time being.

“Singapore is really helping fintech”, says Ned. “Honestly, it’s amazing – the Fintech Festival alone had 40,000 people attending last year. We’re selling to the world, but there’s no better place to do that from than Singapore.”

explore bambu

[Note: The firm’s name was changed to Kindrik Partners in July 2020 and references to the firm’s previous name have been updated.]

working with the hottest tech startups in southeast asia

what our clients say

As entrepreneurs we pour our heart and soul (and blood and sweat) into our companies, and to have someone fighting for us as if it were their own – that’s just awesome!

latest news from kindrik partners

Kindrik Partners advised VC firm Illuminate Financial on its investment in Singapore-based AI-driven data processing and automation company bluesheets. Illuminate led the US$6.5 million series A round. Other returning investors included Insignia Ventures Partners, Antler Elevate, and 1982 Ventures.

Illuminate invests in B2B fintech and enterprise software companies that build solutions for the financial services industry. Backed by global financial institutions such as Citi, JP Morgan, Barclays, Jefferies, Singapore Exchange Group, and BNY Mellon, Illuminate uses its extensive network and industry knowledge to help their portfolio companies achieve their full potential in addition to providing capital.

bluesheets offers AI-driven data processing and workflow automation software that helps businesses digitise and automate their bookkeeping processes. It plans to use the funds to further enhance its AI capabilities and accelerate growth in key APAC markets, including Singapore, Thailand, ANZ, and Hong Kong.

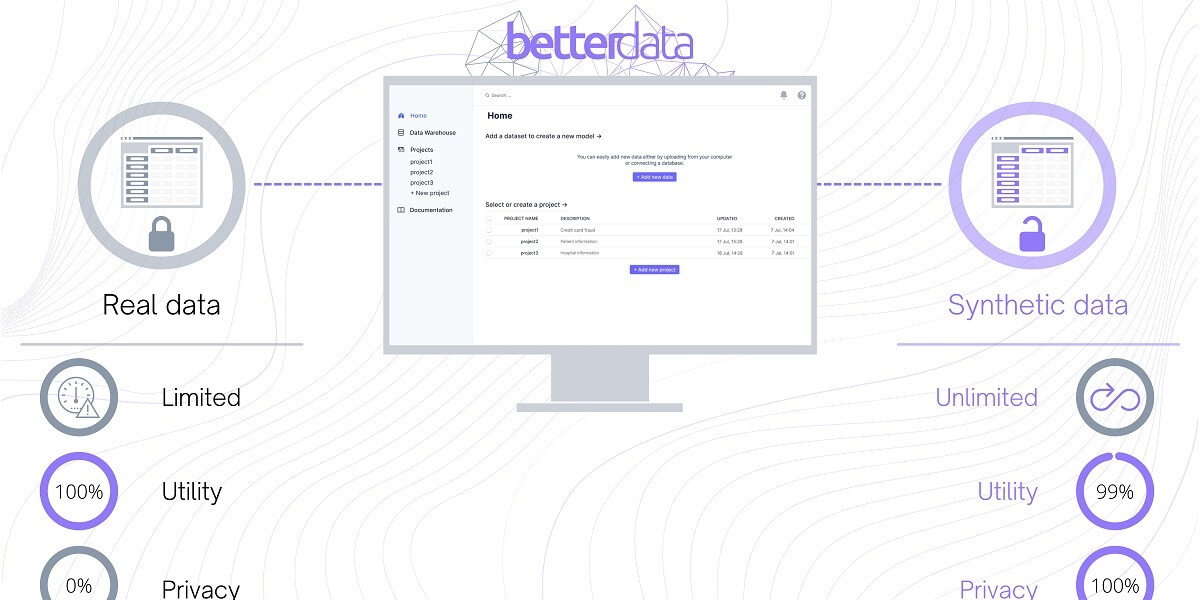

We’re happy to have advised Singapore-based synthetic data company Betterdata on an oversubscribed seed round of $1.65 million, led by Investible.

The company was founded in 2021 by Dr. Uzair Javaid and Kevin Yee and allows clients to share data faster and more securely in compliance with stricter data privacy regulations being introduced around the world. Betterdata uses generative AI to convert real data into synthetic data that looks, feels, and behaves like real datasets. These synthetic datasets retain the structure and correlations of the original data while eliminating the privacy and security concerns that come with holding and sharing sensitive data.

Betterdata plans to use the funding to publicly launch its product, hire more staff as the company scales, and improve its technology stack, with the aim of providing support for single-table, multi-table, and time-series datasets. The company also plans to expand across the Asia-Pacific region over the next two years.